Whether you're a first-time homeowner or years into your mortgage, it’s worth regularly reviewing your home loan to make sure it still works for you. Refinancing gives you the chance to switch to a loan that better meets your needs.

It’s an option more Australians are exploring. According to the ABS, the number of refinances is climbing, with more than 110,000 owner-occupier home loans refinanced in the March 2026 quarter alone.

However, before you dive in, it’s important to make sure it’s the right choice for you.

How does home loan refinancing work?

When you refinance your home loan, you replace your existing home loan with a new one. The new loan is used to pay out the balance of your current mortgage, and your repayments then continue under the new loan instead.

This can be done with your current lender or by switching to a different one. Either way, the original loan is closed and replaced with a new agreement that has its own interest rate, features and terms.

Why you might look to refinance your home loan

-

Lock in a better interest rate

One of the most common reasons to refinance is to secure a lower interest rate. Even a small rate difference could reduce your repayments and the total interest you pay over the life of your loan. If your loan-to-value ratio (LVR) has improved, you may be seen as a lower-risk borrower and qualify for even better rates.

-

Access equity in your home

Refinancing may allow you to borrow against the equity you’ve built up in your property. This can be used to consolidate personal debts or remove mortgage stress, fund home renovations or invest in another property.

-

Remove a guarantor or co-signer

Many homebuyers sign up for their first mortgage with a parent or grandparent as a home loan guarantor to help maximise their chances of approval. Refinancing may give you the opportunity to move to a new loan in your own name if your financial position has improved or your circumstances have changed.

-

Adjust your loan term

Refinancing can also be used to change your loan term. Extending your term may reduce your regular repayments, but it could also increase the total interest you pay over time. Shortening your term may increase repayments but help you pay off your loan sooner and reduce your overall interest.

-

Access additional features

Refinancing can let you access loan features your current mortgage does not offer, such as redraw facilities or offset accounts and more flexible repayment options. This can help you save on interest, manage your cash flow more effectively and give you greater control over how you repay your loan.

When can you refinance your home loan?

There’s no set rule on how soon you can refinance your home loan after you settle it. However, there are several reasons why it’s best to wait at least a year or two before looking to do so.

First, all mortgages come with a range of charges. These can include fees for discharging your mortgage, setting up your new loan with a different lender or, if you’re on a fixed interest rate, exiting your agreement early. This could cost you hundreds or thousands of dollars overall, which might negate the short-term benefit of switching lenders.

Second, each home loan application is recorded on your credit file as an enquiry, which your lender will check. Multiple credit enquiries in a short period can harm your credit score and chances of approval for subsequent loans.

By waiting at least 12 months or more, you’ll give your loan more time to breathe and build up a positive repayment record before moving on to the next one.

Are there better home loans out there for you?

"Refinancing is crucial to ensure you have the best deal on your mortgage. Banks constantly change their rates, policies and promotions, so you never know what you may be eligible for. The best lender for you 12 months ago may be your fifth-best option today. Whether it’s a limited-time cashback, lower interest rate or your circumstances have changed, there’s no harm in seeing what’s out there. Just avoid enquiring with a lender more than once or twice a year to protect your credit score."

How much could I save by refinancing my home loan?

Depending on the size of your mortgage you could stand to save tens of thousands to hundreds of thousands of dollars by refinancing.

To put the potential savings into perspective, here’s how your repayments and overall savings could change on a $500,000 loan with 25 years remaining if you were to refinance from a rate of 6.15% p.a., paying $3,268 a month, to various lower rates:

| Refinanced rate | New monthly repayment | Monthly saving | Overall saving |

|---|---|---|---|

| 6.05% p.a. | $3,237 | $31 | $9,211 |

| 5.90% p.a. | $3,191 | $76 | $22,949 |

| 5.70% p.a. | $3,130 | $137 | $41,120 |

| 5.45% p.a. | $3,056 | $212 | $63,595 |

| Rates are used for illustrative purposes only and aren’t necessarily reflective of the rates you’ll receive on your refinanced home loan. Calculations don’t include additional mortgage break or origination fees. | |||

However, it’s not just the interest rate that impacts the savings on your refinance deal. Other factors include:

- Loan terms: in general, the longer your loan term, the more you’ll pay. When it comes to refinancing, though, having longer left to pay means you may stand to benefit more from switching to a lower rate.

- Loan balance: not only does it cost more to repay a larger home loan, but interest will also be higher. That’s because it’s calculated based on your outstanding balance. If you have two loans with the same interest rate and term but different balances, the loan with the lower balance will cost less.

- Loan fees: you’ll likely have to pay other fees on top of your mortgage’s interest, such as monthly or annual charges, application fees and early termination costs.

- Payment frequency: if you pay half your monthly repayment each fortnight, you’ll effectively make the equivalent of one extra monthly repayment each year, helping reduce your balance and interest faster.

The cost of refinancing your home loan

Before switching loans, it’s important to understand the potential costs involved. You’ll need to pay charges to close your current loan, as well as fees to set up your new one. Depending on your situation, this could cost anywhere from a few hundred to several thousand dollars.

Some common refinancing costs may include:

- Fixed rate break costs, if you’re ending a fixed-rate loan early

- Mortgage discharge fees charged by your current lender

- Application or establishment fees for the new loan

- Property valuation fees

- Government registration or deregistration fees

- Title search fees

Let’s look at an example of someone in New South Wales switching from their current fixed rate mortgage (we’ll call it Mortgage A) to a new variable rate mortgage with a different lender (Mortgage B).

Mortgage A has an outstanding balance of $350,000 and 20 years remaining on its term. The interest rate was fixed at 5.75% p.a. for four years, of which there are two years left to run. Here are the fees someone can expect to pay for refinancing from Mortgage A to Mortgage B:

| Cost | Fee |

|---|---|

| Mortgage A closing costs | |

| Fixed rate break cost | $4,200* |

| Mortgage discharge fee | $400 |

| Mortgage B setup costs | |

| Application fee | $600 |

| Valuation fee | $300 |

| Mortgage registration/deregistration (NSW) | $351.40** |

| Title search fee (NSW) | $18 |

| Estimated total refinancing cost | $5,869.40 |

| * Break cost calculated based on a lender offering a four-year fixed rate of 5.15% p.a. at the time of refinancing. ** Mortgage registration, deregistration and land title search fees are specific to NSW and reflect charges for the 2025–26 financial year. Note: the break cost and discharge, application and valuation fees are all examples for illustrative purposes. You may be charged less or more for each of these when you apply to refinance your home loan. |

|

In this example, refinancing would cost $5,869.40 upfront, so the borrower would need to weigh this against any potential savings from switching loans.

The pros and cons of home loan refinancing

Pros

-

Potential for a lower interest rate

Refinancing may allow you to move to a loan with a lower interest rate, which could reduce your repayments and the total interest paid over the life of the loan.

-

Access equity in your home

Refinancing can let you tap into the equity built up in your property, which may be used for renovations, debt consolidation or other major expenses.

-

More suitable loan features or structure

Refinancing gives you the chance to switch loan types or features, such as moving from a variable to fixed rate loan, adjusting your loan term or accessing features like an offset account.

Cons

-

Refinancing fees and break costs

Refinancing can come with costs, including application fees, settlement fees and mortgage discharge fees. If you’re leaving a fixed rate loan early, break fees can potentially run into the thousands of dollars.

-

You could pay more interest over time

Refinancing to a longer loan term may lower your repayments, but it can also increase the total interest paid over the life of the loan.

-

No guarantee of approval or a better deal

Even if you already have a home loan, refinancing approval isn’t guaranteed. Depending on your financial situation, property value and the lender’s criteria, you may not qualify for a lower rate or more suitable loan features.

How to refinance your home loan with Savvy

-

Apply online

Complete our simple home loan enquiry form.

-

Discuss your options

Your Savvy mortgage broker will help you find the right loan and lender.

-

Submit your application

Your broker will help prepare and lodge your application.

-

Property re-valuation

The lender may check your home’s market value.

-

Get approved

Once your lender is satisfied, your loan will be formally approved.

-

Settle your new loan

Sign documents, settle the new loan and pay out the old one.

Why apply for a home loan with Savvy

The documents you’ll need when refinancing your home loan

The documents you need to refinance are usually similar to the ones you provided when you first applied for your home loan. Your broker or lender will use these to confirm your identity, income, expenses, existing debts and property details.

You may need to provide:

- Proof of identity: passport, driver’s licence, Medicare card, birth certificate or other accepted forms of ID

- Income and employment details: recent payslips (usually your two most recent), tax returns or financial statements if you’re self-employed, plus details of your role and employment length

- Banking and living expenses: recent bank statements (usually from the past 90 days) and details of your regular living expenses

- Current home loan and property details: loan balance and remaining term, plus property information including estimated value, location and ownership structure

- Other debts and liabilities: credit cards, personal loans, car loans or HECS/HELP debt

If you’re refinancing with your current lender, you may not need to provide all of these documents again. For example, they may already have your ID or existing loan details on file. However, they may still ask for updated income, expense or property information before approving the refinance.

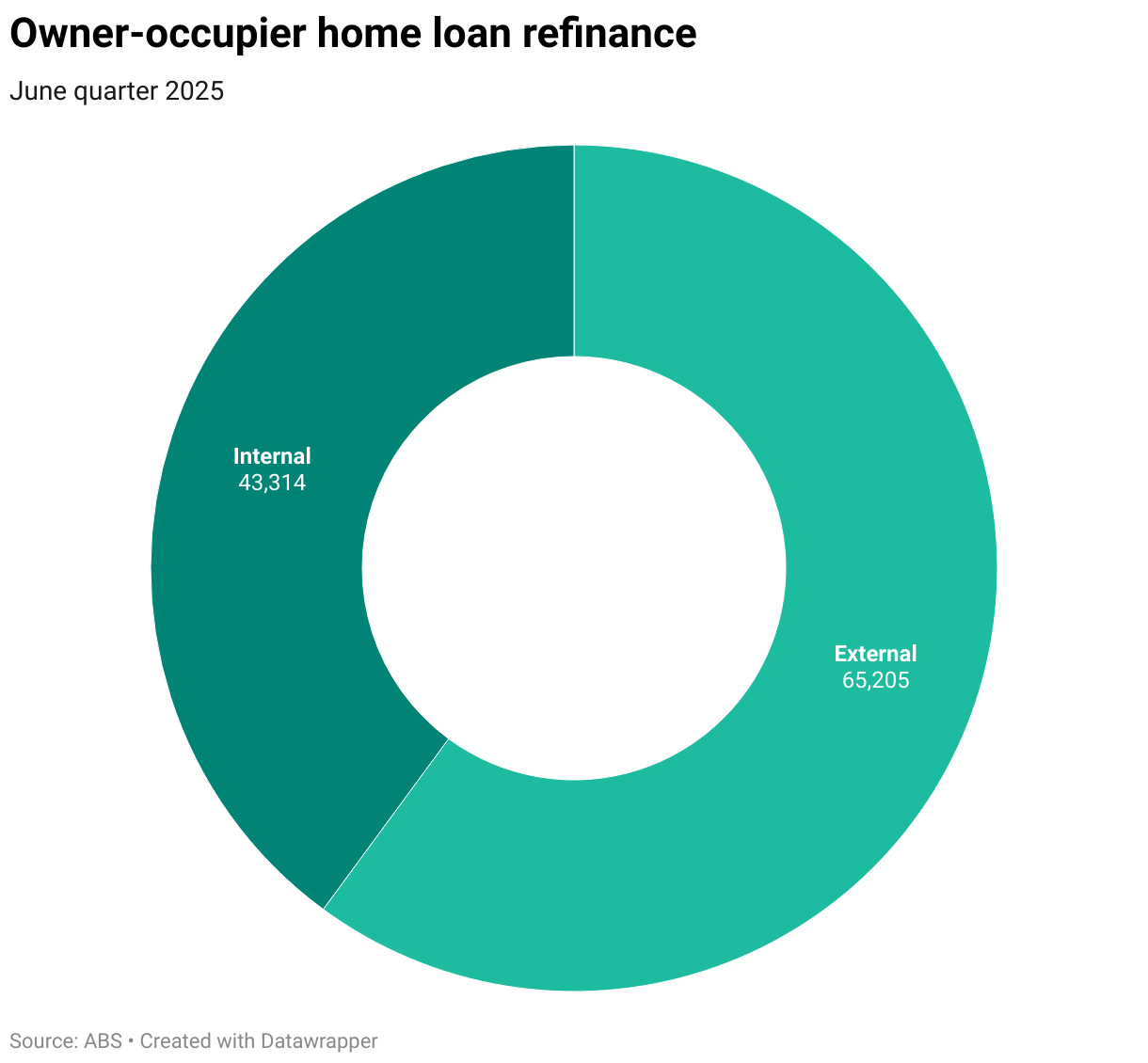

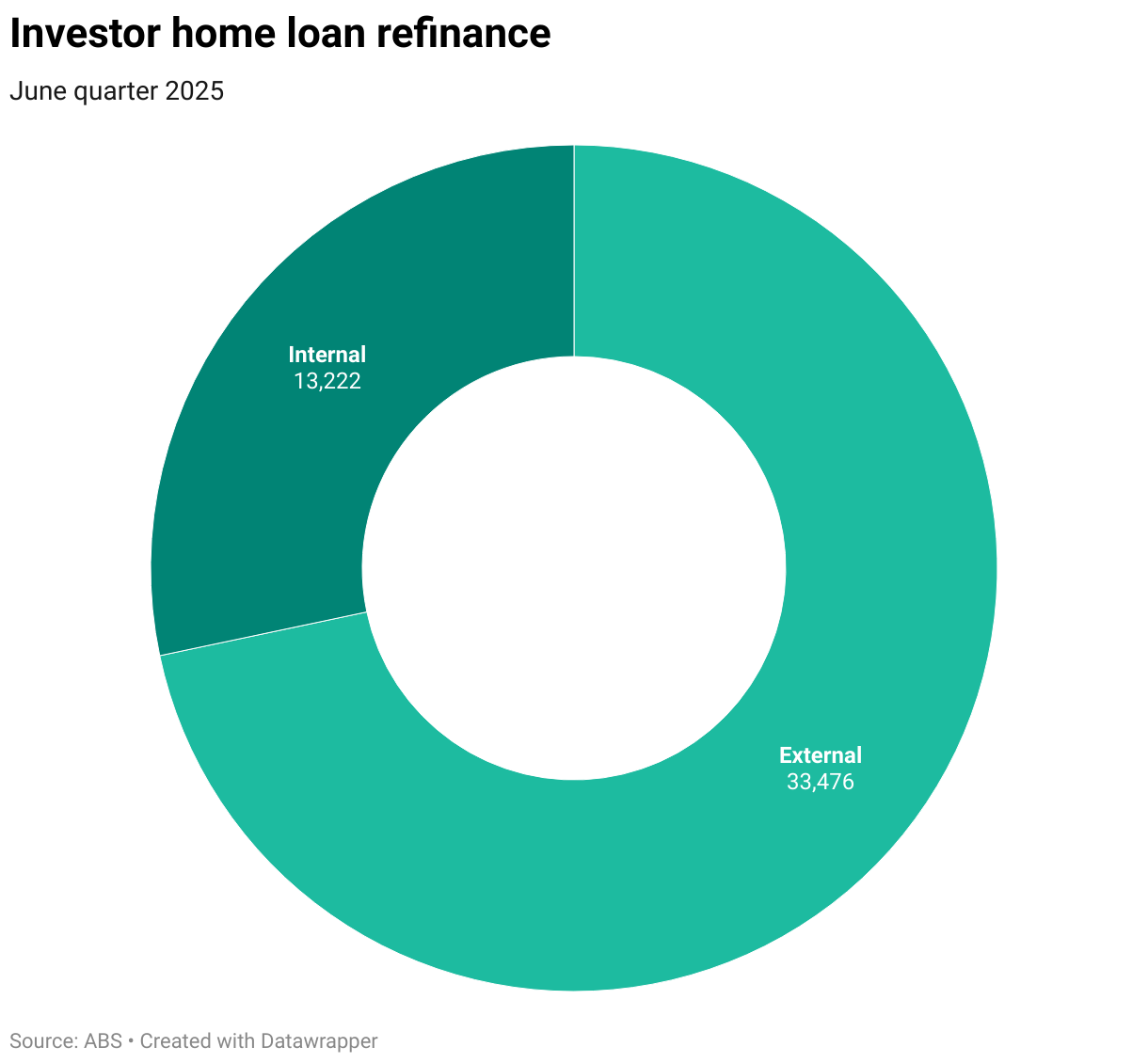

Internal vs external refinancing: which is better?

When refinancing, you have two main options: staying with your current lender (internal refinance) or switching to a new lender (external refinance).

Staying with your current lender is often quicker and simpler, as they already hold your loan and know your history. However, they may not always offer the most competitive rates or the full range of features you’re after.

Switching to a new lender, on the other hand, opens up a wider choice of products and can help you access better rates, features and loan structures, especially if you’re not satisfied with your current loan. However, this option may involve more paperwork and higher costs.

What’s better for you depends on what you’re looking for when refinancing. ABS statistics suggest that more Australians prefer to switch lenders rather than stay with their current one.

In the March 2026 quarter, around 58% of owner-occupiers and 70% of investors who refinanced their home loan switched to a new lender.

Is refinancing my home loan worth it?

Refinancing your home loan can be worth it if it helps improve your situation, for example, if you:

- Are paying a high interest rate and could move to a more competitive home loan.

- Want to reduce your repayments by securing a lower rate or changing your loan structure.

- Want to unlock equity in your property to fund renovations, invest, consolidate debts or cover other major expenses.

- Need different loan features, such as an offset account, redraw facility, split loan, fixed rate or more flexible repayment options.

However, it’s important to ensure the costs don’t outweigh the savings. These can include discharge fees, application fees, valuation fees, settlement fees, government charges and, in some cases, break costs on a fixed-rate loan. In this case, it may be better to stay with your current loan or negotiate a better rate with your existing lender.

It is also worth thinking about how long you plan to stay in your home. If you are planning to sell in the near future, you may not have enough time to recover the upfront costs of refinancing through lower repayments.