Low doc vs standard home loans

| Low doc home loan | Standard home loan | |

|---|---|---|

| Documentation required | Minimal – may include BAS statements, bank statements or an accountant’s letter | Full income documentation such as payslips, tax returns, group certificates |

| Interest rates | Usually higher due to increased risk | Typically lower for borrowers with stable income and good credit |

| Loan-to-value ratio (LVR) | Often capped at 60–80% | Can go up to 95% with lenders mortgage insurance (LMI) |

| Deposit required | Typically a minimum of 20%, depending on the lender | From 5%, depending on credit and LMI |

| Borrowing limits | May be capped, though some lenders allow more | Higher maximums, depending on lender and income |

| Loan features | May still include offset accounts, redraws, fixed or variable rates | Full range of features available |

Who is eligible for low doc home loans?

Low doc home loans are designed for borrowers who don’t have the standard income documentation required for a regular home loan. Those who typically qualify are:

- Self-employed individuals

- Small business owners

- Sole traders and freelancers

You’ll also need to meet all other standard lending criteria, including minimum age and Australian residency requirements.

Documents you need for a low doc home loan

While income documentation is more flexible, lenders will still require alternative paperwork to demonstrate your income. The exact requirements vary between lenders, but commonly accepted documents include:

- Proof of ABN and GST registration

- Business Activity Statements (BAS)

- An accountant’s letter verifying your income

- Bank statements showing consistent income

Low doc home loan deposits

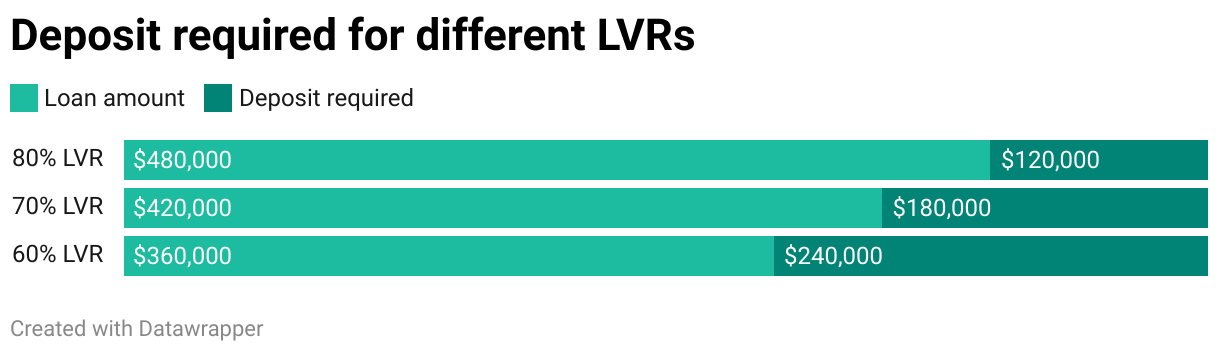

Low doc home loans typically require a larger deposit than standard full doc loans. While traditional borrowers may be able to purchase a property with a deposit as low as 5–10%, low doc applicants usually need to contribute at least 20% of the property’s value upfront because of the higher level of risk involved for lenders.

In some cases, where the borrower’s financial situation is more complex or the lender is particularly cautious, the LVR might be limited to 70% or even 60%, pushing the required deposit even higher. As an example, here’s what the deposit looks like at different LVRs on a $600,000 home loan:

Some specialist lenders may offer low doc loans with a slightly lower deposit, but these often come with stricter terms such as higher interest rates and limited loan amounts.

Why choosing the right lender matters

"It’s key for self-employed borrowers to match their home loan application to a suitable lender. Every lender has slightly different criteria for what they consider a low doc home loan. The difference between just two lenders can easily be a 0.50% variation in the interest rate or an LVR swing of 10%. That could result in a difference of hundreds of thousands dollars over the life of the loan."

Pros and cons of low doc home loans

Key considerations for borrowers without standard income documentation

Pros

-

Accessible for non-traditional earners

Low doc loans offer a home-buying solution for self-employed borrowers or those without standard income documentation like payslips or tax returns.

-

Less paperwork required

You may only need to provide BAS statements, bank statements or an accountant’s declaration.

-

Faster approval in some cases

With fewer documents to verify, the process can be streamlined.

-

Access a range of loan features

Many low doc loans still come with features like fixed or variable rates, offset accounts, redraw facilities and extra repayments.

Cons

-

Lower LVR limits

Most lenders cap LVRs at 80% for low doc loans, which means you’ll typically need a deposit of at least 20%.

-

Higher interest rates

Rates are generally higher to compensate for the increased risk to the lender.

-

Potential for higher fees

Some lenders may charge additional or more expensive fees due to the added risk involved in low doc lending.

-

Limited lender options

Fewer lenders offer low doc loans, which can limit your choices when shopping around for a home loan.

Why self-employed doesn’t mean you need a low doc home loan

Just because you're self-employed doesn't automatically mean you need a low doc home loan. Many self-employed borrowers can still qualify for a standard (full doc) home loan if they have the right paperwork. This includes:

- At least two years of tax returns for your business and personal income

- Business Activity Statements (BAS) or financial statements

- Recent bank statements showing consistent income

- An ABN that’s been active for at least 1–2 years

If you're unsure, a mortgage broker can help you work out whether you qualify for a full doc loan and help you find the best deal for your situation.

Why apply for a home loan with Savvy

Top tips to improve your interest rate

-

Improve your credit score

A higher credit score shows lenders you're a reliable borrower, which can help you access more competitive rates.

-

Put down a larger deposit

The more you contribute upfront, the lower the lender’s risk. This can open the door to lower interest rates and better loan terms.

-

Provide more income verification

Supplementing your application with additional documentation can strengthen your case.

-

Compare lenders

Don’t settle for the first offer you find. A mortgage broker can help you find lenders that offer more favourable rates for low doc applicants.

-

Refinance down the road

If your financial situation stabilises, your business has been trading longer with GST registration or you can provide full documentation, you might be able to refinance to a full doc loan with a lower rate.