Taking out a variable rate home loan can give you more flexibility over how you manage your mortgage. However, it can also mean less certainty over your repayments. Weighing up the potential costs, available features, benefits and risks can help you decide whether this type of home loan suits your needs.

What is a variable rate home loan?

A variable rate home loan is a mortgage where the interest rate can change over time. This means your repayments can go up or down as rates move, often in response to changes set by the Reserve Bank of Australia.

When rates fall, your repayments may decrease, helping you save on interest. However, when rates rise, your repayments can increase, which can put pressure on your budget.

Variable rate loans are often seen as a more flexible home loan option. Many come with features such as extra repayments, redraw facilities and offset accounts, which can help you manage your loan more actively and potentially reduce the interest you pay over time.

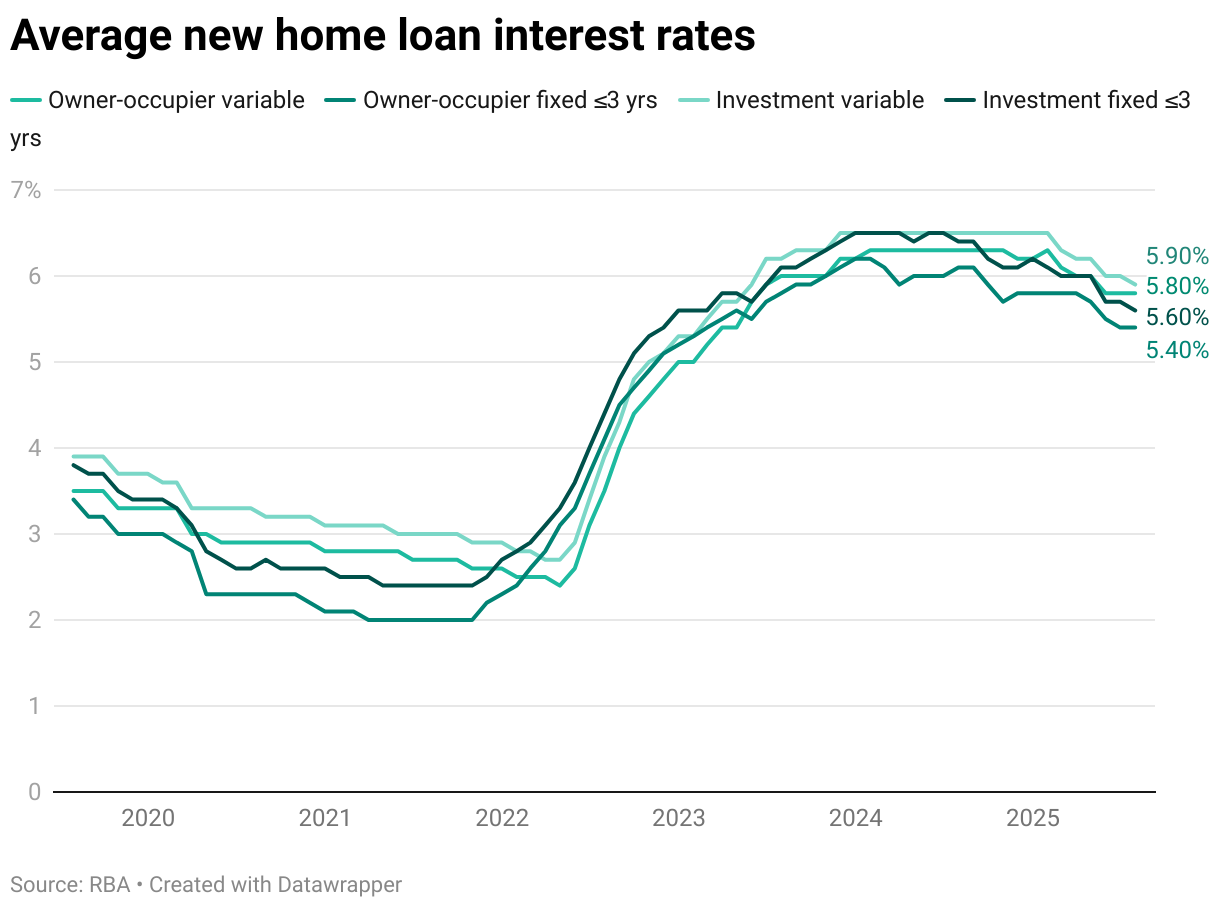

Variable vs fixed rate home loans

A variable rate home loan is different from a fixed rate home loan, where the interest rate is locked in for a set period. Fixed rates can make budgeting easier because repayments stay the same during the fixed term, but they often offer less flexibility and fewer features.

The majority of home loans in Australia are variable rate, with less than 5% of new and outstanding mortgages on a fixed rate, according to the RBA. However, when rates rise, the certainty of fixed rate loans can make them more appealing to borrowers.

Here’s how variable and fixed interest rates compare:

Some borrowers may opt for a split loan, which divides the mortgage between fixed and variable portions. This can provide a mix of repayment certainty and access to flexible features.

How much will my variable rate home loan cost?

The cost of a variable rate home loan can change throughout the life of the mortgage as interest rates fluctuate. Even a small rate change can make a noticeable difference to monthly repayments over time.

To get a sense of how this works in practice, here are example monthly repayments for a $500,000 home loan over 30 years:

| Interest rate | Estimated monthly repayment |

|---|---|

| 5.50% p.a. | $2,839 |

| 6.50% p.a. | $3,160 |

| 7.50% p.a. | $3,496 |

You can estimate how much a change in rates would impact your home loan with Savvy’s home loan repayments calculator.

The exact rate you’re offered will depend on factors such as your credit history and financial profile, loan amount, deposit size, property type and the lender’s pricing and eligibility criteria.

It’s also important to consider the comparison rate, which includes both the interest rate and most standard home loan fees, giving a clearer picture of the loan’s true cost.

What do 2026 rate rises mean for variable rate home loans?

In May 2026, the RBA lifted the cash rate by 0.25 percentage points to 4.35%. This was the third rate rise of 2026, bringing the cash rate back to where it was before rate cuts in 2025.

As with previous rises earlier in the year, many variable rate borrowers can expect higher repayments following this latest increase as lenders pass on the cost.

For example, on a $650,000 loan over 30 years, a rate rise from 6.50% to 6.75% would increase repayments from around $4,108 to $4,216 per month, an increase of about $108 per month or $1,296 per year.

The Big 4 banks are split on where rates will move next. Commonwealth Bank and ANZ expect rates to hold steady at the next RBA meeting in June, while NAB forecasts another increase. Westpac also expects rates to rise again this year, although it is less certain that another increase will happen in June.

Given the uncertainty around where rates may move next, borrowers considering this type of loan should think about whether their budget could comfortably handle further increases in repayments if rates continue to rise.

Can I make extra payments towards my variable rate home loan?

Yes, most variable rate home loans allow you to make extra repayments on top of your minimum repayments. Paying extra can help reduce your loan balance faster and potentially save on interest over time.

If you’re able to consistently pay more than the minimum, you may also be able to pay off your loan sooner and reduce the total interest paid over the life of the loan.

Many variable rate loans also include flexible features that support this, such as:

- Offset accounts: this is a transaction account linked to your home loan. Any money in the account is offset against your loan balance, meaning you’re only charged interest on the reduced amount.

- Redraw facilities: if you’ve made extra repayments, a redraw facility allows you to access those additional funds later if needed. This can provide a safety net for unexpected expenses, although access rules vary by lender.

While offsets can help you reduce interest, they typically attract fees up to $300 per year, which is why it's important to check the comparison rate.

While extra repayments are common on variable rate loans, it’s important to check whether any limits, fees or conditions apply before you start paying more.

The pros and cons of variable rate home loans

Pros

-

Repayments may fall if rates decrease

If interest rates drop and your lender passes on the decrease, your repayments may fall. This can lower your regular mortgage costs and reduce the amount of interest you pay over time.

-

Access to additional loan features

Variable rate loans often come with features such as offset accounts and redraw facilities, which can help you manage your money and reduce interest costs.

-

Extra repayment flexibility

You can usually make additional repayments without penalty, helping you pay off your loan faster and reduce the total interest charged.

-

Easier to refinance or switch loans

Variable loans generally offer more flexibility if you want to refinance, switch lenders or restructure your home loan.

Cons

-

Repayments can increase

If interest rates rise, your monthly repayments may increase. This can affect your budget and make it harder to manage other costs.

-

Less repayment certainty

Because variable rates can change over time, it can be harder to predict your long-term repayment amounts compared to a fixed rate loan.

-

Potential for mortgage stress

If rates rise quickly, repayments can increase within a short period. This may put pressure on your budget and make it harder to stay on top of regular expenses.

Is a variable rate home loan right for me?

A variable rate home loan may suit borrowers who want flexibility and are comfortable with repayments changing over time, rather than having fixed certainty.

It may work well if you want the ability to make extra repayments, use features like offset accounts or keep the option to adjust or refinance your loan in the future. It can also suit borrowers who are comfortable with some movement in repayments and can manage changes in their budget if rates rise or fall.

On the other hand, it may not be ideal if you prefer stable, predictable repayments or would find increases in repayments difficult to manage within your budget. In that case, a fixed rate loan may feel more secure.

How to apply for a variable rate home loan with Savvy

-

Complete our online form

Tell us about yourself and how much you want to borrow.

-

Supply your documents

Provide us with the info and documentation we need to verify your profile.

-

Talk to your broker

Your Savvy specialist will give you a call to discuss your home loan options.

-

Get pre-approved

We’ll let you know how much you’ve been pre-approved to borrow.

-

Find a property

Put in an offer on the property you’ve chosen and have it accepted.

-

Formal approval

We’ll submit your formal application for approval.

-

Settlement and sign-off

Once settlement’s complete, the property is yours!

Why apply for a home loan with Savvy

What our customers say about their finance experience

Savvy is rated 4.9 for customer satisfaction by 7300 customers.

Home loan lenders you can compare