What is a first home buyer home loan?

A home loan for a first-time buyer as a product is no different from any other home loan. You’ll still be paying a deposit, having a portion of your home purchase covered by the bank and repaying that debt with interest and fees in set instalments throughout your loan. However, the key differences lie in rebates and governmental support programs, which aren’t available to existing buyers or investors.

Home loan jargon explained for first-time buyers

Given you’re in the process of looking to buy your first home, there’s a good chance that, between speaking to a real estate agent or mortgage broker, you’re going to come across a few terms you’ve never heard before.

- Borrowing power: an estimate of how much you may be able to borrow based on your current financial profile. Your lender will give you an idea of this figure when you get pre-approved for your loan. You can also use Savvy’s borrowing power calculator to find out an estimate of what your borrowing power may be before applying.

- Comparison rate: a percentage figure which shows borrowers a truer cost of the loan when additional loan fees have been taken into account. A comparison rate must be displayed alongside all loan interest rates under Australian consumer protection law. These additional fees may be loan application fees or account-keeping charges.

- Deposit: a lump sum you’ll need to provide as a contribution to the purchase price of your home. Most lenders require 20% of the purchase price to avoid paying lenders mortgage insurance (LMI), but first home buyers may be able to pay as little as 5% in certain circumstances.

- Interest-only (IO) loan: a type of home loan whereby the borrower only pays the interest due on the loan for an initial set period (typically between one and five years) and doesn’t make any repayments towards the principal sum borrowed. This is most commonly used by investors.

- Lenders mortgage insurance (LMI): an insurance premium that borrowers may have to pay if they can’t provide a 20% deposit. This protects the lender in case of loan default and can amount to thousands of dollars, although there are ways around paying LMI even if you don’t have a 20% deposit (which we’ll discuss a bit further down).

- Loan-to-value ratio (LVR): a percentage figure that describes how much money you want to borrow compared to the value of the property you want to buy. For example, if you pay a 20% deposit on your home purchase, that means the LVR is 80%.

- Principal: the loan you’re borrowing or applying for.

- Principal and interest loan (P&I): this is a standard home loan. Your loan repayment consists of both the interest due on the loan and a small amount of the sum you originally borrowed. As time goes by, interest decreases and a larger portion of each repayment goes towards paying off your principal.

- Split loans: involve one portion of the loan having a fixed interest rate and the remaining portion having a variable interest rate. The borrower can choose which portion of their mortgage is fixed and variable (commonly 60/40 or 70/30).

- Stamp duty: a state-based tax on the price of buying land. First home buyers can get reductions and exemptions in many states. If not, it can amount to tens of thousands of dollars.

Why apply for a home loan with Savvy

First home buyer schemes, grants and cash incentives

Most states and territories in Australia have rebate and incentive schemes for first home buyers, as well as several programs that are available Australia-wide. These include:

Australian Government 5% Deposit Scheme

The Australian Government 5% Deposit Scheme, formerly known as the First Home Guarantee, is a program that allows eligible first-time buyers to pay as little as 5% as a deposit without being charged LMI by their lender. The scheme now has unlimited places available and no upper limit on your income.

The types of property you can buy are:

- Existing house, townhouse or apartment

- House and land package

- Off-the-plan apartment or townhouse

- Vacant land with a separate building contract

This program is only available for properties that are purchased under the approved price caps for each state and territory, which the Australian Government updated in October 2025. These caps are as follows:

Australian Government Help to Buy Scheme

The Australian Government Help to Buy Scheme is another program being rolled out in December 2025. Under this program, first-time buyers can enter a shared equity agreement with the Government to reduce the size of their home loan and pay as little as 2% for their deposit. You can hand up to 40% of your home's equity to the Government for new builds or up to 30% for existing homes.

The Government's share in your home must be repaid at market value either in voluntary instalments, as a lump sum or when you sell your home. For example, let's say you buy a $1 million home in Sydney and use the Scheme to give the Government 30% equity in your home. If you sell your home in five years' time and its value has increased by 20%, you'd have to repay $360,000 to the Government, rather than the $300,000 its share was worth when you bought your home.

Unlike the 5% Deposit Scheme, places are limited to 10,000 per year for the Help to Buy Scheme and income caps are in place ($100,000 for singles and $160,000 for joint applicants or single parents). The location-based price caps are the same, with the exception of reducing Sydney and NSW regional centres' upper limit to $1.3 million. Central Coast, Mid-North Coast, Coffs Harbour-Grafton and Richmond-Tweed are also added as NSW regional centres.

First home super saver (FHSS) scheme

The FHSS scheme allows eligible first-time buyers to make voluntary superannuation contributions which can then be used towards their deposit. You can contribute up to $15,000 per year and up to $50,000 overall via this scheme.

The main benefit of utilising the FHSS scheme is that concessional contributions are taxed at a rate of 15%, which is much lower than standard tax rates outside of super. On top of this, any assessable FHSS amounts are subject to a 30% tax offset.

According to the ATO, when you’re ready to buy your home, you can withdraw the following:

- 100% of your eligible personal voluntary contributions you haven't claimed a tax deduction for (non-concessional contributions)

- 85% of your eligible salary sacrifice contributions (concessional contributions)

- 85% of eligible personal voluntary super contributions you have claimed a tax deduction for (concessional contributions)

- An amount of associated earnings on both concessional and non-concessional contributions

If you’re considering using the FHSS scheme, it’s worth investigating it further or speaking to an accountant or tax professional to determine whether it’s right for you.

First Home Owner Grant (FHOG)

Each state and territory has its own FHOG, with the exception of the ACT. Here’s the breakdown of what it looks like where you live:

Stamp duty concessions

On top of the FHOG, eligible first-time buyers can also receive an exemption from, or reduction to, their payable stamp duty. Here’s how that looks in each state or territory:

How much do I need for a deposit as a first home buyer?

As mentioned, lenders will require borrowers to pay a deposit of at least 20% when buying a home to avoid paying LMI. However, there are several ways around this. Here are some examples of different deposit situations for a $500,000 home purchase, paid with a 30-year loan at 5.50% p.a.:

Scenario #1: paying a 20% cash deposit

The most straightforward solution, a 20% deposit will meet all lenders’ requirements and spare you from having to fork out for LMI. It also means your loan will be smaller at just $400,000 (80% LVR) in this situation. In this case, you’d be paying $1,048 per fortnight and $417,221 in interest overall.

Scenario #2: paying a 10% cash deposit and LMI

If you aren’t in a position to reach the 20% deposit mark or take advantage of any other programs, you’ll likely be forced to pay LMI. Not only would your fortnightly loan payments and total interest rise to $1,179 and $469,374, respectively, with a 10% deposit, but you’d also have to deal with a potential LMI bill of over $8,000.

Scenario #3: paying a 5% cash deposit with First Home Guarantee

Being approved for the FHG means you won’t have to worry about LMI and can be approved with a deposit of just 5%. In this scenario, that’s just $25,000 cash. With a $475,000 loan, you’d be paying $1,244 per fortnight and $495,450 in total interest. It’s important to note that because of the smaller deposit through FHG, you’ll have to show that you can still afford to service the loan.

Scenario #4: paying no cash deposit with a guarantor

The last option is applying with a guarantor, aka the bank of Mum and Dad. This is usually a parent or grandparent who has enough equity in their property to act as partial security for 20% of your loan. Depending on your lender and your guarantor’s financial profile, you could be approved for a loan worth 100% of your property’s value. In this situation, your fortnightly repayments would be $1,310 and your overall interest bill would be $521,526. No LMI is payable on a guarantor loan.

First home buyer tips

Budget is king

"Buying your first home isn’t just about the numbers; it's about strategy. The right home loan sets the foundation for your financial future. First-time home buyers will often overlook expenses like stamp duty, LMI and moving costs, which can really stack up.

Find out what incentives or schemes you can utilise, how much you should aim to contribute as a deposit and how to decrease unforeseen overheads.

Most importantly, get pre-approved! You’ll know exactly what your budget is and can search for your dream home with confidence."

Building inspections can save your bacon

"When I was buying my first home, I put in an offer on an older house that was accepted, subject to a building and pest inspection.

I sought out a licensed operator to carry out the inspection, who found a range of red flags that a regular person like myself couldn’t have picked up on. Because of the clause in the contract, this was enough for me to back out of the deal without any financial pain.

While it’s hard to get your deposit together, keeping enough funds aside for a check like this undoubtedly saved me tens, if not hundreds, of thousands of dollars in the long run."

Don’t sleep on offset accounts

"When my partner and I were applying for our home loan, we had two main priorities: we wanted a competitive interest rate and an offset account. I had run the calculations long before we found our house and saw just how much we could save with even a relatively modest amount in the bank.

So, when we did eventually find the place that was right for us, we were straight in for the offset package. Our lender allowed us to create unlimited accounts, so we essentially moved all our banking over and created nominal transaction, savings and joint accounts.

Because neither of us put in 100% of our savings, we were able to throw the amount left over into our accounts and reduce the total interest we’d have to pay by over $100,000. That could make a huge difference when it comes to buying our forever home."

How to apply for a home loan as a first-time buyer

-

Apply online

Fill out our online form with all the necessary details.

-

Send documents

Supply your broker with the required documentation.

-

Speak to us

Talk with your broker and personalise your loan to your needs.

-

Conditional approval

From there, pre-approval allows you to shop within your budget.

-

Secure your home purchase

Once you've found it, lock in your first home of choice.

-

Formal application and approval

Your broker will guide you through the process, from formal application to full approval.

-

Settlement

Once everything's signed off, you’ll officially be a first home buyer!

First home buyer statistics: 2025

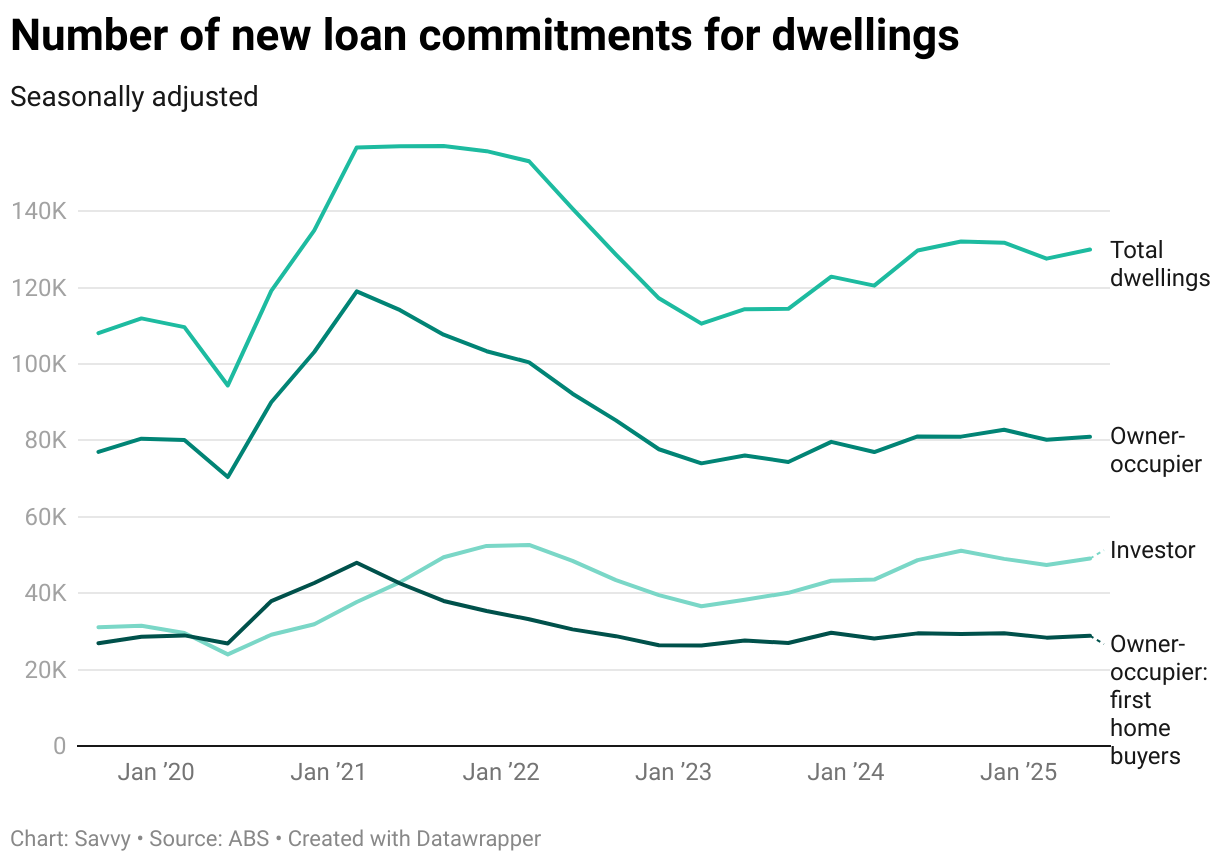

- The number of home loans taken out by first-time buyers rose by 1.7% in the June 2025 Quarter compared to the March 2025 Quarter, but fell by 0.2% compared to the June 2024 Quarter, according to ABS data.

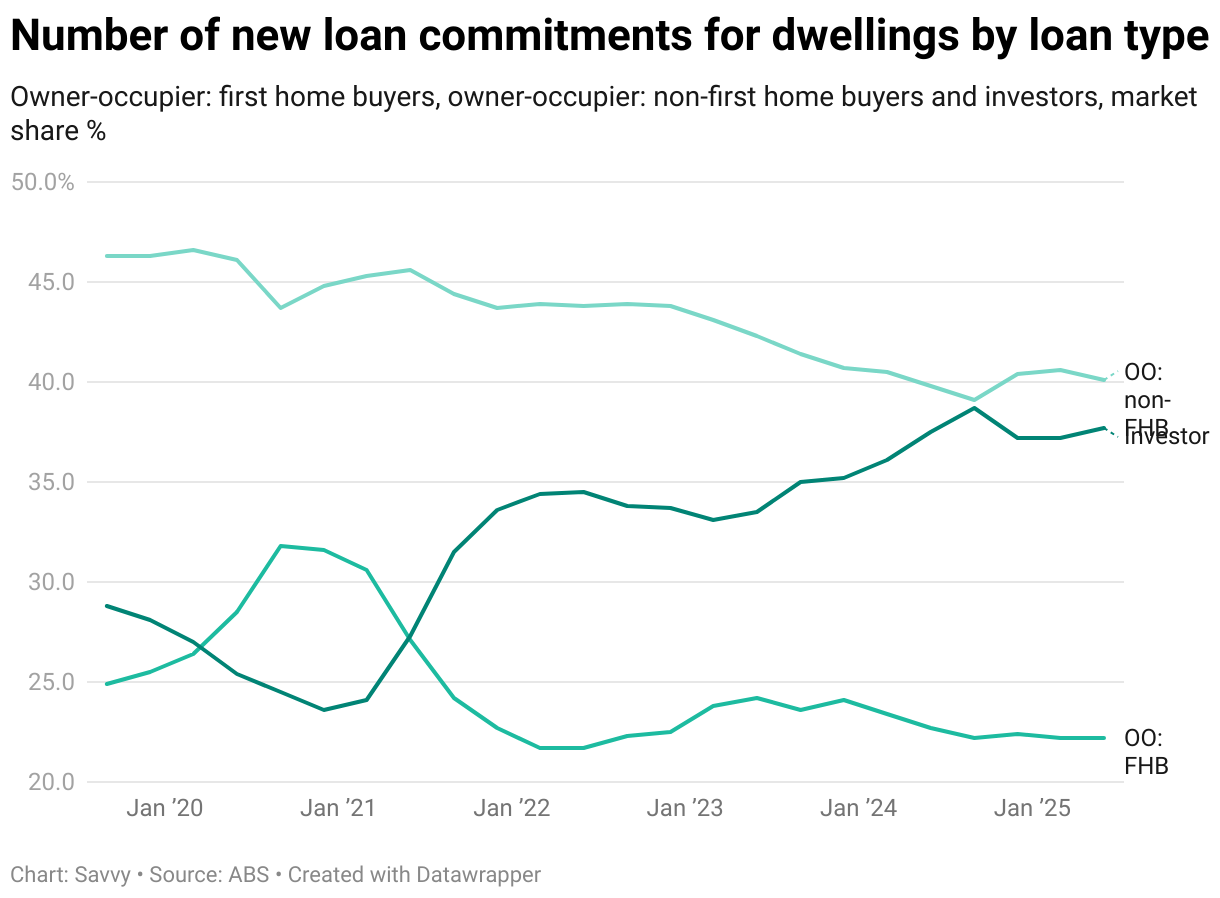

- The 28,861 home loans approved for first-time buyers in the June 2025 Quarter represented 35.7% of owner-occupier mortgages and 22.2% of all home loans in that period.

- The value of home loans taken out by first home buyers was $16.3 billion in the June 2025 Quarter, representing an increase of 5.7% compared to the March 2025 Quarter and a 2.2% increase on the June 2024 Quarter.

- Per a recent Mozo study, Australian parents are gifting an average of $74,000 to help their kids buy their property, which has gone up by $4,000 since 2021.

- The same study found that 75% of parents who lend their children money to buy their property don’t want it repaid.

- Housing Australia reported that one in three first home buyers made use of the Home Guarantee Scheme across the 2023-24 financial year.

- A UBS survey of 1,000 Australian adults found that the second most common purpose of supplying money to adult children was for mortgage or debt repayments (28%), behind only living expenses (56%).

- Finder research shows that 70% of all first home buyers in 2025 won’t save up for a 20% deposit before buying their home.

- One third of new buyers (34%) didn't take out their home loan with their usual bank, while a quarter (24%) are searching for their home in a different region or state to where they currently live.

- In 2025, 17% of first home buyers say they received money from their parents, up from just 11% in 2022.

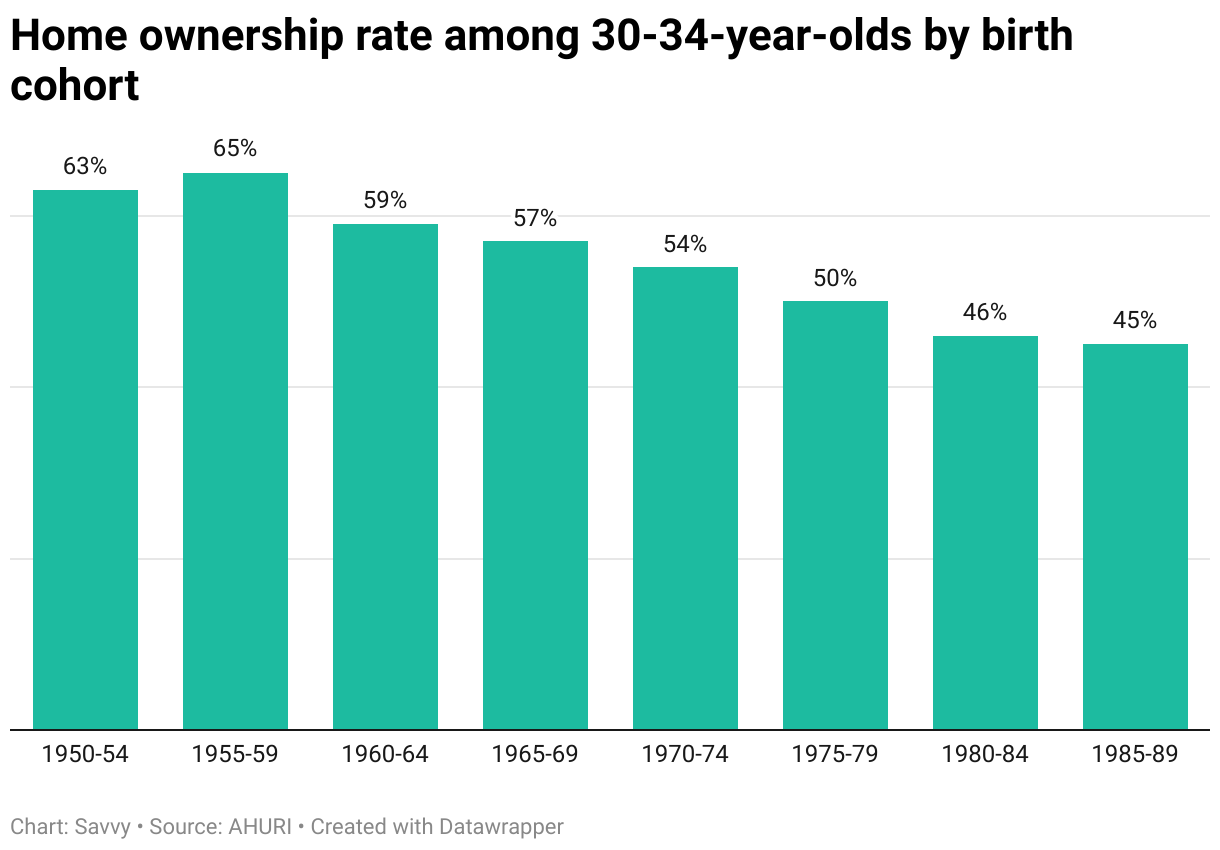

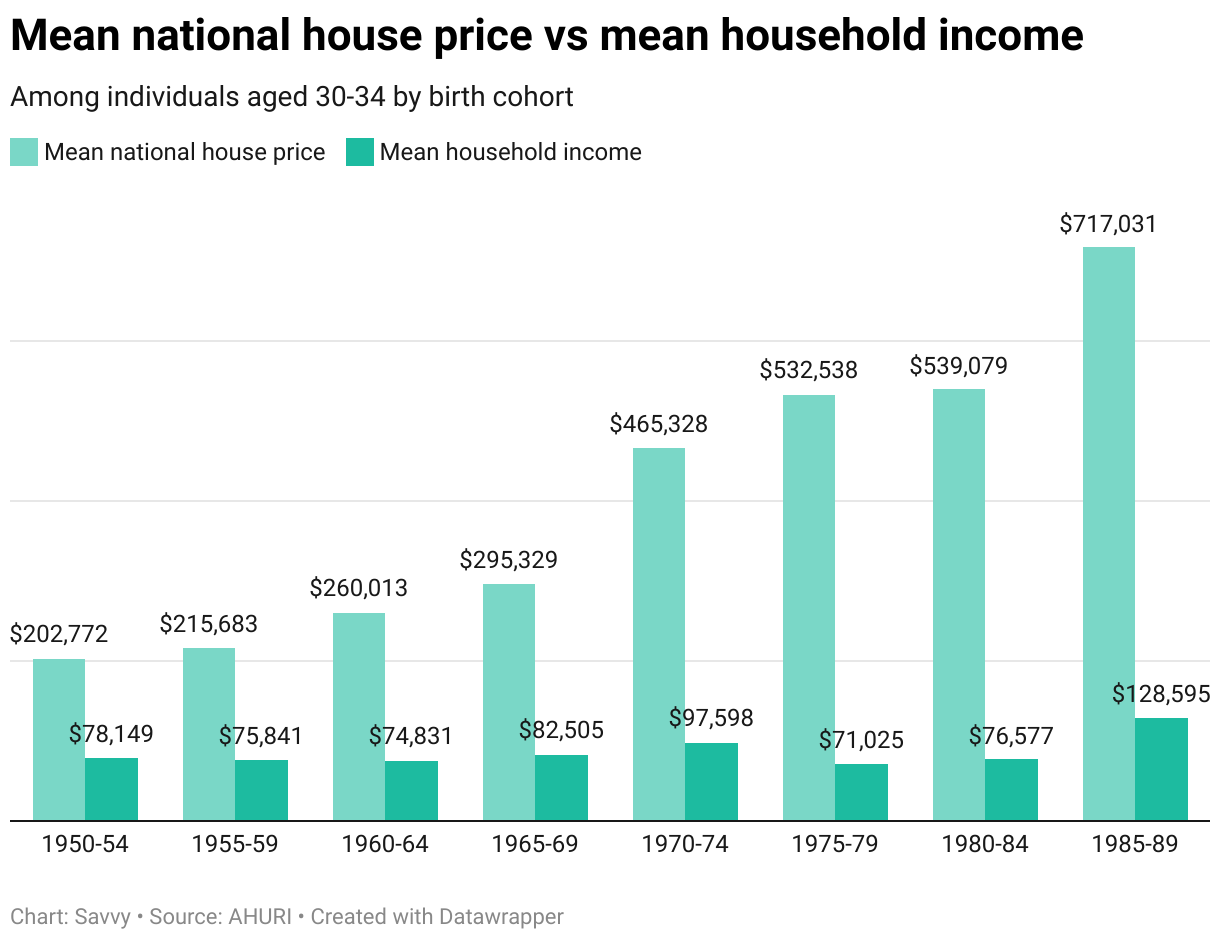

- Research released by the Australian Housing and Urban Research Institute (AHURI) found that only 45% of 30 to 34-year-olds owned property between 2015 and 2019, compared to the peak of 65% of those in that age bracket between 1985 and 1989.