- The Savvy Promise

At Savvy, our mission is to empower you to make informed financial choices. While we maintain stringent editorial standards, this article may include mentions of products offered by our partners. Here’s how we generate income.

In this article

With RBA interest rates at all-time lows, house prices skyrocketing and inflation on the rise, interest rates look set to inevitably rise during 2022. Savvy’s analysis of the latest data provides insight for homeowners regarding mortgage stress and potential increases in home loan repayments.

- 4.2% increase in house prices in Q4 2021

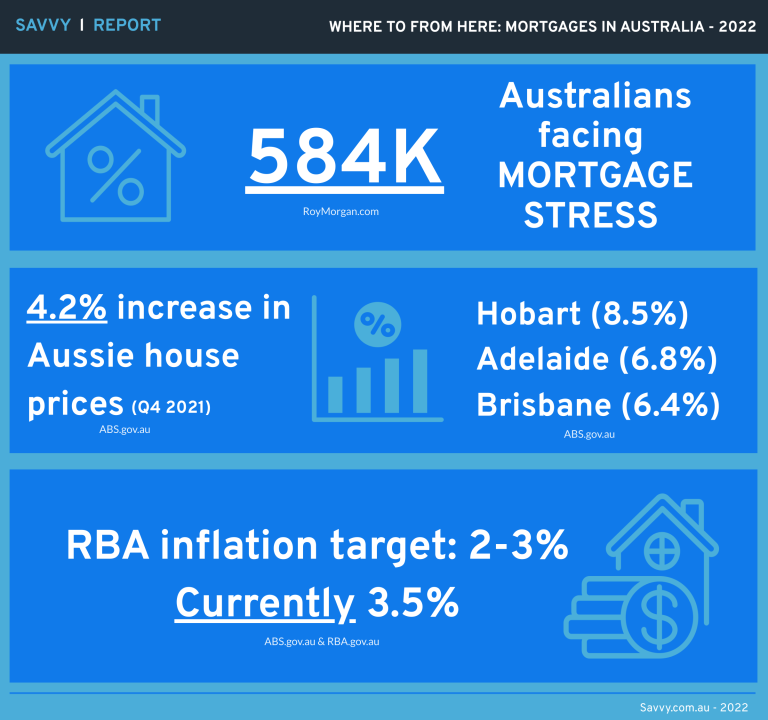

- 584,000 mortgage holders at risk of mortgage stress at the end of 2021

- With official cash rate at 0.10%, Interest Rates will inevitably go up

- RBA inflation target is between 2-3%: currently 3.5%

Despite credit crunches, Royal Commissions into the Banking and Finance Sector, and a global pandemic, Australians are undeterred from buying houses. Whether it’s to own and occupy or as an investment, outstanding mortgage debt has increased year on year since 2011 according to Statista – even over 2020 and 2021 when the pandemic and uncertainty was at its peak.

Can this be explained as simply as Australians taking advantage of record low interest rates?

Nothing lasts forever – and the cheap money to gobble up housing assets needs to be taken up as quickly as possible, as far as the broader public is concerned. For those on variable rates, what does that mean when the interest rates rise? What does that mean for inflation? What about house prices? We look into mortgages in Australia 2022, and where Australia goes from here.

Residential Mortgages

The value of all residential mortgage debt in Australia as of 2021 is an apt A$2,021.3 billion – comprised of $1,333.5 billion held by owner-occupiers and $687.8 billion held by investors. This has been on a steady increase since 2011, where the volume of debt (combined) was at $1,211.5 billion with the only outlier being 2018-2019, where the levels remained much the same; $1,808.1B vs $1,813B.

2019 may have seen owner-occupier and investors both trying to wait out lower interest rates. For owner-occupiers (on average), waiting a year from July 2019 to July 2020 represented a dip of 0.62%p.a. (3.84% in July 2019, 3.22%p.a. in July 2020) and a further 0.35%p.a. to 2.81%p.a. by July 2021.

Investors (on average) could have saved 0.73%p.a. waiting a year from July 2019 to July 2020 (4.31%p.a. vs 3.58%) and another 0.43%p.a. (3.15%p.a.) to July 2021.

Value of owner-occupier and investor mortgage debt outstanding in Australia from 2011 to 2021 (in billion Australian dollars)

No Data Found

https://www.statista.com/statistics/1209476/australia-value-of-mortgage-loans-outstanding-by-type/

Inflation and house prices

In the December Quarter 2021, dwelling purchase prices by owner-occupiers rose in all capital cities by 4.2%, according to the ABS. The highest price rises were recorded in Hobart (8.5%), Adelaide (6.8%) and Brisbane (6.4%.)

This is due to the underlying inflation the ABS recorded in Q4 2021. Fuel costs rose by 6.6% due to an increased demand for oil across the world. Shortages of labour and raw materials also drove prices of housing. This is the underlying inflation – the inflation in fuel and construction must be passed on to consumers through increased prices for goods and services. The Master Builders Association says that there may be a widespread timber frame shortage by 2035 if timber plantations are not expanded.

Despite this, purchases of dwellings for owner-occupier homes increased by 7.5% in December 2021 (annual trend.)

Commercial Mortgages

As of February 2022, small business interest rates stand at 4.14%p.a. (on average), 2.59%p.a. for medium business, and 1.51%p.a. for large business for outstanding loans.

New loans attract an average interest rate of 3.55%p.a. for small business, 2.37%p.a. for medium business, and 1.29%p.a. for large business.

Historical Interest Rates in Context

For many Australians, they can remember when the Reserve Bank of Australia official cash rate hovered at above 10% – 17.5% during 1990. During the 1990s and 2000s, the cash rate oscillated between about 7% and 5% – the only real major change coming during the Global Financial Crisis of 2007-2008, when the rate crashed from 7% to 3 % in a matter of six months.

From November 2010 until December 2012, the rate stayed above 3%. The “new normal” of interest rates staying below 2% began in April 2016, tumbling even lower in July 2019 to 1%.

In October, it was below 1% – 0.75%. It was cut even further to 0.5 and 0.25% in March 2020, in response to the emerging COVID-19 pandemic and economic uncertainty.

The unthinkable was made real in November 2020, when the RBA set the official rate at just 10 basis points – 0.10% – a record low in Australian financial history.

Average owner-occupier and investment mortgage interest rate in Australia from July 2019 to December 2021

No Data Found

https://www.statista.com/statistics/1209498/australia-average-mortgage-interest-rate-by-type/

Mortgage Debt – is it sustainable?

In a speech to the Responsible Lending and Borrowing Summit in 2018, Assistant RBA Governor Michele Bullock said that despite high levels of mortgage debt, the financial system’s ability to absorb a widespread increase in financial stress levels was adequate and would remain stable if borrowing remained responsible.

Ms. Bullock did note in her speech that a large percentage of investor interest-only loans will expire between 2018-2022, leaving two groups at risk – those who may find switching to interest and principal repayments difficult to manage, while another smaller group will experience financial stress.

Interest Rates and Inflation

Interest rates and fractional reserve banking, which Australia uses much like the US and UK, are dependent on a central bank setting cash rates and inflation targets. The cash rate is the official lending rate that the central bank charges banking and lending institutions, or as the RBA calls it “interest rate on unsecured overnight loans between banks.” One of the RBA’s levers against rampant inflation is increasing the interest rates – this theoretically decreases the amount of money in circulation, which causes prices of goods and services to stop rising faster, hopefully past the point where wages or interest on bank deposits can keep up.

The RBA sets an inflation target of between 2-3%. According to the Australian Bureau of Statistics, the Consumer Price Index (CPI) which tracks inflation rose by 3.5% year on year (December 2020 to 2021) due to higher dwelling construction costs and automotive fuel prices. This is the highest “underlying” inflation since June 2014.

The Elephant in The Room: The Inevitable Rise of Interest Rates

As inflation increases, the Reserve Bank of Australia will have to increase interest rates. This may be a welcome boon for long-suffering savers, who might see a bit more interest gained on their deposits. However, as mentioned if inflation outpaces interest on deposits, the purchasing power of your dollar weakens.

That means coming up with more money to service a home loan – or any type of credit product.

In a simple scenario, if you borrowed $500,000 over a 25-year loan term with a variable interest rate of 2.7% (the average as of December 2021), your monthly repayments would be about $2,294. Let’s also assume your combined average income is $135,720 (the average wage in Australia multiplied by two).

|

Interest Rate |

2.7% |

2.95% |

3.2% |

3.45% |

3.7% |

|

Repayment |

$2,294 |

$2,358 |

$2,423 |

$2,490 |

$2,557 |

|

Extra per year |

$0 |

$768 |

$1,548 |

$2,352 |

$3,156 |

|

Income % towards mortgage |

20.3% |

20.8% |

21.4% |

22% |

22.6% |

If wages (as a whole) rose in proportion with inflation, this may not be a big a problem as it seems. However, according to the ABS, the Wage Price Index only rose by 2.3% over Dec 2020 to Dec 2021.

If a household is on the average income (described above) and gains a mere 2.3% pay rise, that means $3,121.56 extra income per year.

If that household experiences a 1%p.a. increase in interest rates, they will need to come up with $35 per year to accommodate the mortgage. This may hardly register as a blip in the family budget and could be absorbed with little effort.

However, if that family does not get a pay rise at all, they would need to come up with the figure shown in the table above – i.e., a 1% rise means $3,156 extra on the mortgage per year. That is more easily said than done for many Australians.

If the same family loses a significant amount of work hours, or is suddenly on a single income due to a shock job loss, this would immediately place them in mortgage stress – a situation where a household spends more than 30% of their earnings on servicing a mortgage.

Bill Tsouvalas, Savvy Managing Director & home finance expert;

“According to Roy Morgan, an estimated 584,000 mortgage holders were at risk of mortgage stress at the end of 2021, which is a near “record low” according to the polling agency: mortgage stress was down significantly from a year prior. This is after numerous government interventions such as extended payment holidays, JobKeeper/JobSeeker, COVID Disaster Payments, and so on.

With record levels of government debt on the books now, the government – and whatever that government might be after the May 21 Election – will be reluctant to bail out homeowners in view of creating even more inflation.

What is pleasing to note is that unemployment is at near-record lows (4%), which should push wages higher, especially in services where employers are scrambling to fill positions.

If you are a homeowner and haven’t fixed your rates, the time to act is now. Refinancing at a lower rate is also better to start sooner rather than later. Because with all indicators pointing to rising inflation, rates will definitely start shifting upwards."

This information is general in nature and not a substitute for professional financial advice.

For more information, contact Adrian Edlington – [email protected]

Statista.com - Australian Average Mortgage Interest Rate by Type

Statista.com - Australia Value of Mortgage Loans Outstanding by Type

ABS.gov.au - Consumer Price Index Australia - Latest Release

Masterbuilders.com.au - Australia Faces Timber Deficit of 250,000 house frames in 15 years

TradingEconomics.com - Unemployment Rate

Did you find this page helpful?

Written by

Written by

Author

Adrian Edlington Commentary by

Commentary by

Guest Contributor

Bill TsouvalasPublished on April 14th, 2022

Last updated on March 18th, 2024

Fact checked

This guide provides general information and does not consider your individual needs, finances or objectives. We do not make any recommendation or suggestion about which product is best for you based on your specific situation and we do not compare all companies in the market, or all products offered by all companies. It’s always important to consider whether professional financial, legal or taxation advice is appropriate for you before choosing or purchasing a financial product.

The content on our website is produced by experts in the field of finance and reviewed as part of our editorial guidelines. We endeavour to keep all information across our site updated with accurate information.