- The Savvy Promise

At Savvy, our mission is to empower you to make informed financial choices. While we maintain stringent editorial standards, this article may include mentions of products offered by our partners. Here’s how we generate income.

In this article

Mortgage stress is becoming the go-to term for individuals or families who are devoting over 30% of their income towards a mortgage and suffering financial hardship as a result. Other industry bodies, categorise mortgage stress on a spectrum.

- The common definition of mortgage stress is any mortgage holder that is using over 30% of their income on mortgage repayments.

- A Savvy Survey (2021) showed 26.9% of homeowners are experiencing mortgage stress.

- Mortgage stress can also take its toll on mental health and relationships. – You can combat mortgage stress by auditing your expenses and making some adjustments to your spending and lifestyle.

- If you are experiencing mortgage stress or fear you will miss a mortgage repayment, there are many ways to get help.

What is mortgage stress?

Mortgage stress is also referred to as ‘rental stress’ and ‘housing affordability stress’ in some media outlets.

According to the Australian Banking Association, as of February 2021, more than 80,000 people in Australia are still deferring their home loan repayments due to financial stresses, some due to financial difficulties incurred by state government responses to the COVID-19 pandemic. In Victoria, where almost all businesses were closed for over 112 days, the deferral rate is the highest at 31%.

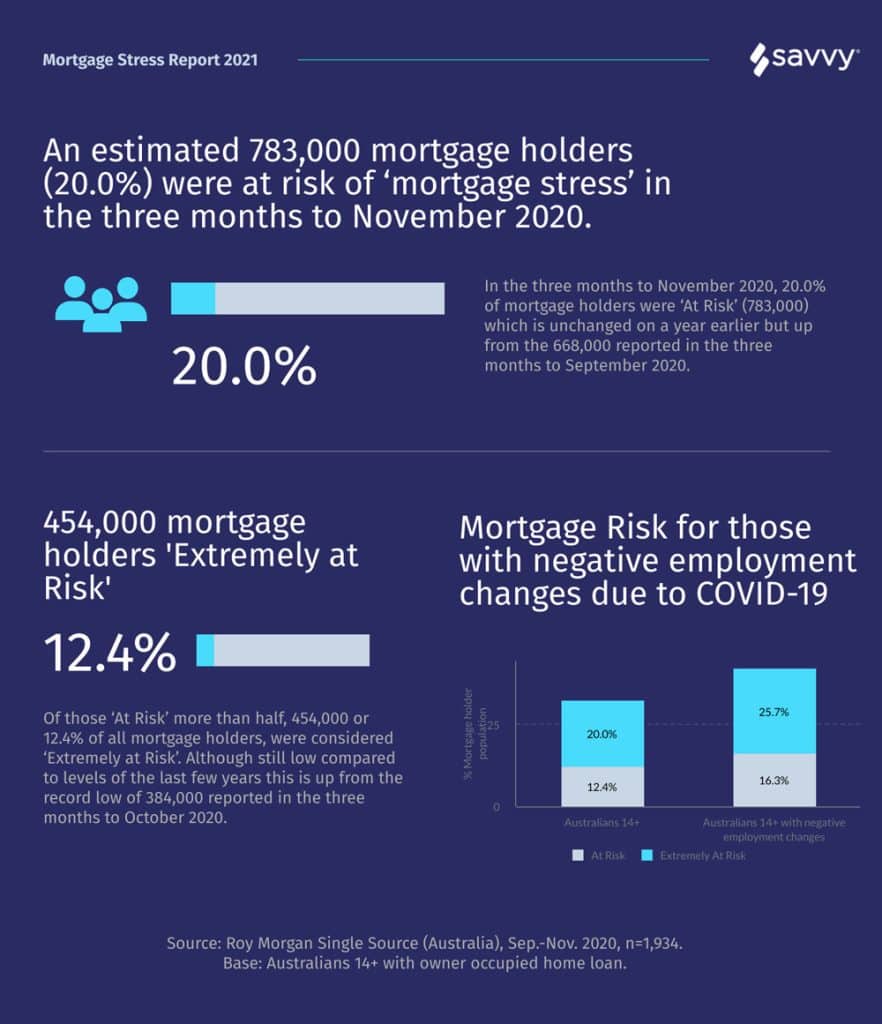

Roy Morgan Research places homeowners directing between 25% and 45% of their income toward their home loan as “At Risk” while homeowners spending over 45% of their income on their home loan is declared “Extreme Risk.”

At the end of 2020, 783,000 mortgage holders are considered “At Risk” with 454,000 considered at “Extreme Risk.”

Savvy’s own Housing Affordability Survey conducted in March of this year showed 26.9% of homeowners experiencing mortgage stress.

The latest statistics from Digital Finance Analytics show that 40.2% mortgage borrowers may be in mortgage stress, with 2.8% in default. The highest demographic segment is “Young Growing Families” (73.2%) followed by “Battling Urban” (65.3%) and “Disadvantaged Fringe” (61.9%). This “stress” is not only financial but mental and emotional, as we’ll explain later on.

Signs of mortgage stress

The first signs of mortgage stress may come in the form of not having enough money to spend on luxuries or disposable items such as a night out, lunches, take-away coffee, etc. Your children may have to forgo school excursions or camps as you can no longer afford them.

Mortgage stress may also manifest itself when you suddenly need to come up with a lump sum of money due to an unforeseen expense such as a medical bill, car repair, or appliance replacement. You may have no other recourse but to pay for it using a credit card, borrowing money from friends or family, or asking for an advance from your employer. You may have taken out a small personal loan to cover these expenses. This can compound mortgage stress as you’ll be required to pay back these debts which you may not be able to afford.

The most obvious sign of mortgage stress is living paycheque to paycheque and juggling expenses in order to pay them on time – or even waiting for utilities and other bills to become overdue so you can scrape together the money to pay the bill.

If you have recently lost your job or had your hours reduced, this can also place you or your family in mortgage stress. Even if you have fallbacks such as superannuation or income protection insurance, the shortfall in your income can place you in an At Risk category.

It can also affect your mental and physical health, as well as your relationships (see more below.)

Discovering the numbers behind mortgage stress

You may have the feeling of being under mortgage stress – but without evidence, a feeling is just a feeling. To know for sure, you’ll need to do a thorough look at your finances to determine if you actually are suffering a “textbook definition” of mortgage stress.

First, you will need to create a snapshot of all your income and expenditures over the last three months (at least – you can create a larger timeline if you wish.) You should break down your expenditures into categories such as your mortgage repayments, other debt repayments, transport, groceries, utilities, school fees/education, work expenses, entertainment, savings, etc.

Then you will get closer look at where all your money is going and whether 25% of your income is going directly toward covering your mortgage. If you find that less than 25% of your income is going directly toward your mortgage repayments each month, you can use this opportunity to make savings by cutting spending from other areas.

How you can stop mortgage stress before It occurs

If you have run the numbers and find that you or your household is running close to the 25-30% of total income being put toward your mortgage, you can help stop mortgage stress before it occurs.

- Downsize

If you are paying a mortgage on a home with three bedrooms and two bathrooms and are only a couple with no immediate plans for children, you may want to consider downsizing to a smaller place instead. Smaller places are always cheaper, and you can funnel your equity into purchasing a new home with a corresponding lower principal. This can dramatically decrease your repayments and put you back in black.

- Renting Out Rooms

Though you may think your housemate days are behind you, if you have a room or two spare that are underused or not used at all, consider renting them out and putting the rent towards your mortgage repayments. This effectively splits the mortgage repayments between your boarders or housemates and frees up your income for savings, debt repayments or extra repayments.

- Debt Consolidation

If you have many small outstanding debts such as credit cards or personal loans, you may want to consider consolidating your debts under one loan and one repayment. This can free up your cash to devote to your home loan if you are experiencing temporary cash flow problems such as reduced hours or are injured and cannot work.

- See A Financial Adviser

According to Savvy’s Financial Literacy Survey conducted in February 2020, almost 80% of respondents said they had never consulted a financial adviser. A financial adviser can not only help you make the most of your income but also grow your wealth for the future. They may identify areas where you could relieve mortgage stress that you may not have thought of.

- Reduce Expenditures

Now that you have a snapshot of your finances, you need to start reducing your expenditures – even if you are planning to downsize, take on a boarder, consolidate debts, or see a financial adviser. By identifying where your money goes, you can rein in disposable expenditures such as extra take away coffees – a 250g pouch of ground coffee costs about $12 and can last three weeks. Making a coffee and taking it with you before going to work could save you $80 a month (provided you buy $4 coffees) or $960 a year. For some, that is almost a full month’s mortgage repayment.

- Switch To Interest Only Payments

Almost all mortgage repayments pay off a combination of your interest and principal. However, you can for a time pay only the interest on the loan, which usually means lower repayments. Be warned; after the interest only period ends, you will be faced with higher repayments. The interest rate may also be higher than a comparable principal and interest loan. You’ll also forgo building up equity in your home for that period.

- Ask for a Hardship Variation

If you are struggling to meet payments your lender is obligated under the National Consumer Credit Code to consider a hardship variation if you have a reasonable cause, such as sudden illness or unemployment.

A hardship variation can come in many forms such as extending your loan period making repayments more manageable; a “repayment holiday” or postponement for a short period; a mixture of the two; or a postponement of payments until you sell your home. Your lender can refuse your variation, but they must give you suitable reasons. If you are unsatisfied with their decision, you can apply to the Australian Financial Complaints Authority for an independent review. This review is free of charge.

Refinancing your way out of mortgage stress

As of 2021, the RBA official cash rate stands at 0.1% – the lowest in Australia’s financial history. If you are on a fixed rate mortgage, you may be paying more in interest than you need to. The same goes for variable rate loans – your lender or bank may not be “passing on” the rate cut, which means you are paying more in interest and by extension, repayments each month.

If you have not reviewed your home loan in at least two years, you may want to consider refinancing your loan to make smaller repayments or savings in interest. Some refinance options may keep your repayments the same while reducing the time it takes to pay off your mortgage overall. This is great for saving money long-term, but doesn’t necessarily alleviate your immediate mortgage stress.

You need to talk to a broker or financial adviser to determine whether the cost of the refinance – break fees, establishment fees, etc. will leave you in a better position than the original loan. Other factors to consider are added features – perhaps your refinance loan will give you an offset account, which can reduce the amount of interest you pay on your loan.

What should I do if I’m about to miss a mortgage payment?

If you do not have enough money to pay for your mortgage or are considering covering your repayment with an alternative credit source such as a credit card or cash loan, you should contact your bank or financial institution immediately.

After 30 days of non-payment, you will officially be in arrears. Being in arrears (behind) is not the same as default, but one can lead to the other. The illion Mortgage Nation Report for 2020 found that Australia has $20.4 billion worth of home loans in arrears.

If you are worried you will go into arrears, banks and lenders have a professional obligation under responsible lending practices to help you through financial hardship. You may be granted a temporary extension, a hardship variation, or repayment holiday to help you catch up.

You must intervene as quickly as possible before getting too far behind. If you miss multiple mortgage payments, this can put you at risk of default. This is when a mortgage holder falls behind on repayments by over 90 days or more (about three months.)

At 60 days, some credit reporting agencies will record a default on your credit history, which can lower your credit score and potentially disqualify you from accessing competitive interest rates if you wish to refinance or other credit products such as credit cards or personal loans in the future.

Mortgage stress and relationship stress

Mortgage stress can cause friction among couples and families and contribute to declining mental health. United States research firm Ramsey Solutions in 2017 released a study showing 41% of couples with more than $30,000 in consumer debt fight about money, compared to only 25% of debt-free couples.

The Australian Psychological Society in studies have shown personal finance stress is one of the main sources of stress for Australians. In fact, 49% of people on average have poor mental health due to personal financial issues.

Having enough money can help people feel safe, stable, and secure. Mortgage stress can cause “arguing with the people closest to you about money, having trouble sleeping, feeling angry or fearful, mood swings, tiredness, loss of appetite, and withdrawing from others.”

If you are fearful about your mental health or the mental health of loved ones with mortgage stress, please seek help:

National Debt Help Hotline: 1800 007 007

The Department of Human Services: Crisis and special help page.

Lifeline: 13 11 14

Did you find this page helpful?

Written by

Written by

Author

Thomas Perrotta Commentary by

Commentary by

Guest Contributor

Bill TsouvalasPublished on May 18th, 2021

Last updated on March 19th, 2024

Fact checked

This guide provides general information and does not consider your individual needs, finances or objectives. We do not make any recommendation or suggestion about which product is best for you based on your specific situation and we do not compare all companies in the market, or all products offered by all companies. It’s always important to consider whether professional financial, legal or taxation advice is appropriate for you before choosing or purchasing a financial product.

The content on our website is produced by experts in the field of finance and reviewed as part of our editorial guidelines. We endeavour to keep all information across our site updated with accurate information.