- The Savvy Promise

At Savvy, our mission is to empower you to make informed financial choices. While we maintain stringent editorial standards, this article may include mentions of products offered by our partners. Here’s how we generate income.

In this article

Lending data – known as the lending indicators – is published each month by the Australian Bureau of Statistics. It shows us all the relevant Australian borrowing statistics – including mortgage commitments, personal loans, and business loan commitments across different categories.

In this analysis, we will be focusing on changes in mortgage and business loans and what it means for home buyers, investors, and business.

In May 2021, housing loan commitments, or people who wanted and were approved for a home loan, rose by 4.9%, only to fall 1.6% in June. More strikingly, personal fixed term loans, such as for cars, consolidating debts, or other types of personal investments rose by 5.6% only to experience a 12.6% drop over the next month. Business construction loans, a type of loan the Australian Bureau of Statistics calls a “volatile” series, dipped by approximately 20% over the two-month period.

What’s interesting is that new loan commitments had been rising unabated until June 2021 – excluding people refinancing their loans. The amount of total new home loans financed in May 2020 was $16.66 billion. They’ve more than doubled at $32.57 billion a year on – a new overall high, eclipsing the previous peak of $22.68 billion in May of 2017, only now receding for the first time in 13 months.

By providing up to date research, we will make sense of all the data – including insights into what it all means by expert economic and financial analysis from Dr. Diaswati Mardiasmo, Ph.D and Savvy Managing Director Bill Tsouvalas. This will dive deep into the background of why Australia is experiencing such consistent lending highs and a narrowing of the gap between investor and owner-occupier loans – a “perfect soup” of conditions, as Dr. Mardiasmo calls it.

Household Lending

Owner Occupier

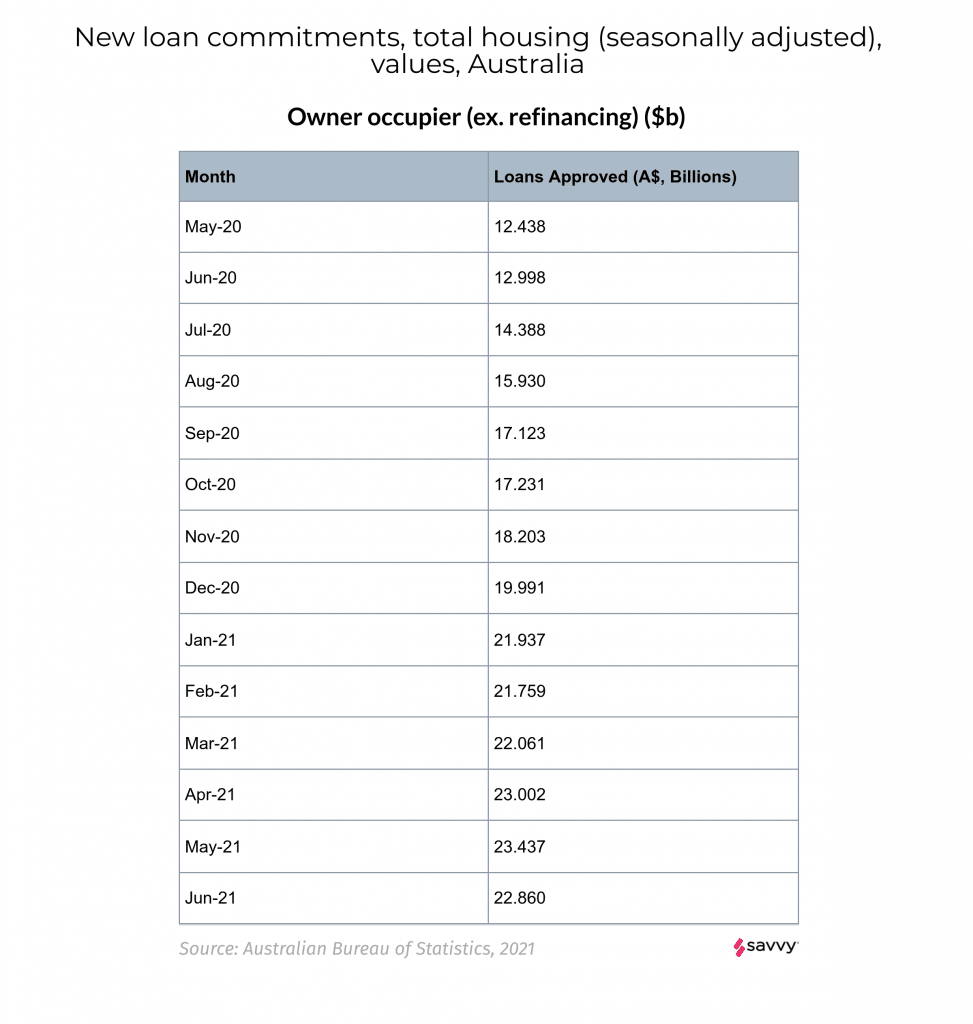

Owner occupier lending almost doubled over the last 12 months, reaching a series (series being the range of data on offer by the ABS – in this case, May 2003 to May 2021) peak of $23.48 billion in owner-occupier loans, only to drop for the first time in June 2021. In seasonally adjusted terms, this indicated a rise of 1.9%.

Investor

Investor mortgages followed the same trend as owner-occupier loans, ending up at a six-year high of $9.13 billion in May 2021. The previous peak was April 2015 ($10.08 billion). This was a significant increase of 13.3%. Curiously, the average gross rental yield for all types of houses, averaged around the country, remained steady at 3.9% according to SQM Research. This one indicator may not explain the surge in investor mortgages – this will be explored in detail later in the article.

Business

Property Acquisition

In the business sector, property buying had a precipitous drop compared with the previous month’s peak of $6.57 billion in loans approved – May 2021 saw a 27% fall to $4.79 billion, only to rebound; surpassing the April high and reaching $7.160 billion. It’s a far cry from the 12-month low of July 2020 of $3.2 billion; but a curious trend emerges with any “splurge” month – new loans fall off considerably the month or two after any large increase.

Construction

Unusually for the construction side of business, new loan commitments levelled off at about $2.36 billion, before dropping to $1.9bn in June. The construction business loan market has wild swings and roundabouts – for example, in October 2012, construction loans hit a massive peak – $4.42 billion – while the next month contracted to a quarter of that size – $1.1 billion.

Analysis

Looking at the States

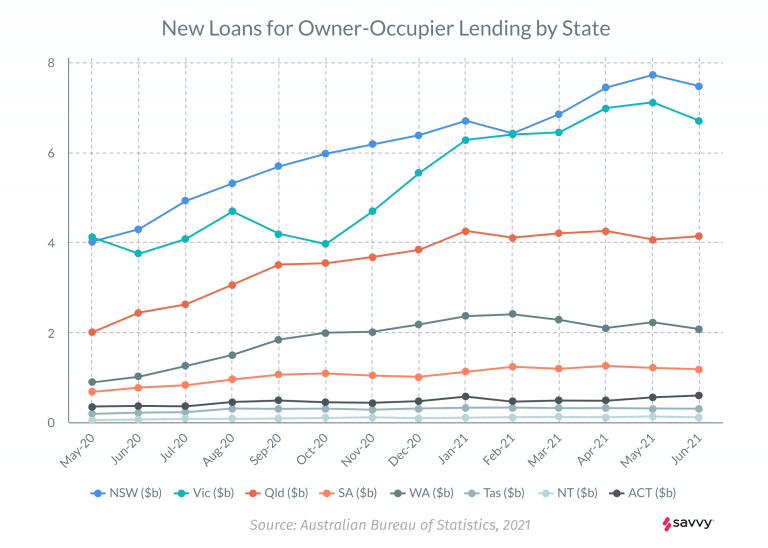

As to be expected, New South Wales is the breakout leader in owner-occupier lending, peaking at $7.716 billion in May with Victoria close behind at $7.109 billion – being the most populous states, this isn’t unusual. All have tracked upwards in the last year, beginning May of 2020 at over half value of lending. The ABS says that the eight capital cities’ property prices rose 5.4% this quarter, a 7.5% increase over the last twelve months. The recent dips from the lofty May highs could indicate a turning of the tide, or simply a correction.

The outlier seems to be Western Australia, which has an approximate population to South Australia (1.7 million). Perth’s house prices, according to the Real Estate Institute WA (REIWA), were “the lowest median house value in any capital city in Australia” – which has seen a flock of people buying rather than renting in Perth. They estimated a rise of 6% to 10% in house prices over 2021.

Housing Finance by Purpose

Existing Dwellings

New South Wales and Victoria saw significant rises in the value of new loan commitments for the purchase of existing dwellings – loans approved for existing dwelling purchases surged to $17.2 billion, far and away the leading reason for taking out a mortgage loan.

Construction

Construction of dwellings dipped by 2.3% in May compared to the month previous, totalling $3.13 billion. (then down to $2.59 bn in June 21. This was down from a series peak of $4.04 billion in January of this year.)

New Dwellings

The purchase of new dwellings (just constructed, ready to move in) fell by 2.3%, – the third month of negative growth in a row, according to the May 2021 ABS Lending Data. This may be due to the reduction of the HomeBuilder grant from $25,000 to $15,000 in January of this year.

First Home Buyers

The amount of owner-occupier lending to first home buyers shrank by 0.8% in seasonally adjusted terms, although Victorian and NSW first home lending remains at historic highs. Owner-occupier first home lending accounted for 32.7% of all owner-occupier loans – approximately $7.67 billion worth of loans. The number of first home buyers stood at 13,869 in June, down from a January 2021 peak of 16,257 (seasonally adjusted).

Renovations

Renovation lending has surged in the last year, going from a low of $216 million in August 2020 to a near-series peak of $453 million in May.

Investing

New South Wales and Victoria have led the climb all around, accounting for 70.2% of all investor lending in May 2021.

Taking out third place is Queensland, standing at about half the total of Victoria – and a third of NSW’s lending. This could be partially explained by property prices in NSW, where the median house prices have climbed to over $1.3 million in the Greater Sydney area.

Commentary

“A Perfect Soup” of Conditions

According to Chief Economist at PRD Real Estate, Dr. Diaswati Mardiasmo, Ph.D, the current climate of government stimulus, low interest rates, and a narrow gap between owner-occupier and investment loans has “stirred the pot” when it comes to the current surge in lending.

“The climb has started actually from when we were hit with COVID, because the government came out with schemes such as HomeBuilder,” she says. “HomeBuilder came at the same time as us having historical low interest rates. The cash rate has been kept the same at 0.1%. You've got that very stable base.

“Banks are offering very low interest rates, big first home buyer interest rates. In combination between what's happening in the interest rate market and also governments stimulus in terms of increasing home ownership access, those two have worked together in terms of them resulting at the end of it, pushing up the amount of lending that is being granted and the people who are now eligible to gain funding for buying homes, such as the First Home Buyer guarantee.”

No matter the demographic, people are eager to buy no matter what.

“We all know that property transactions are at the highest in most places,” Dr. Mardiasmo says. “We've seen record breaking sales. We've seen anecdotal evidence of agents saying that properties were flying out of the door, they're getting multiple inquiries, all of those sorts of things. But all of that worked hand-in-hand; the evidence is there that people are definitely buying more. Whether you're a first home buyer, owner-occupier, or investor, everyone is transacting more.”

Locking In the Low Rates

Variable rate home loans are the most popular type of loan, with approvals topping $28.6 billion in May 2021. However, the gap between fixed and variable loans has narrowed, with fixed rate loans coming in at $24 billion. This month’s result was the gap between variable rate loans and fixed rate loans in March 2020 – $24.71 billion. Savvy’s Managing Director Bill Tsouvalas says that home buyers want to lock in the historically low interest rates. “It makes sense to hedge your bets and lock in the lowest interest rates this country has ever seen, or ever will see, for as long as possible,” he says. “If you can lock in while the RBA cash rate is at 0.1%, or at least partially lock your mortgage in at that rate, it’s a no brainer. There’s little wonder why the gap has tightened to such a degree since the pandemic began.”

A Redirect from Elsewhere?

Unsurprisingly, personal finance for funding travel and holidays has been close to nil since the Federal Government banned international travel from March 2020, in response to the COVID-19 pandemic. In April 2020, only $2 million of loans were issued – a record low across the entire series. In May 2021, $7 million in loans were approved for travel – which is a drop in the ocean compared to housing and other personal finance commitments. Across April-May 2021, there was another peak in the Household and Personal Goods indicator, with approvals reaching $100 million over both months. This overtook the previous peak in January 2020, which stood at $92 million.

Safer Than the Bank – Houses for Investors

Investing in homes is now more attractive due to higher rental yields, low returns from deposits, and a narrowing gap between investor mortgages and home owner mortgages. Dr. Mardiasmo says that “It's not quite the same, but it is very close at the moment. Previously, there used to be a bigger gap between home loan rate for investors and home loan rates for owner occupied. But at the moment, that gap is actually quite narrowing and it's very small. Investors see this and they kind of go, ‘Okay, well, investor loans are currently at the lowest point, so it makes sense to invest.’

“People who are seasoned investors know that this would be the best time to get that loan on a much lower repayment and almost for the same rate as homeowners.”

Vacancy rates are also plummeting; addressing the rental shortage by offering new sources is a guaranteed winner, according to Dr. Mardiasmo.

“We're seeing vacancy rates of only one point something percent; under 2%, under 3%. Some of them are at 0.4, 0.6% in Tasmania. These are numbers that we haven't seen before. Investors see that chance. Vacancy rates are continuing to fall; it's tight. Rental yields are definitely going up because of the shortage in the rental market.”

Australian Bureau of Statistics, August 2021, Lending indicators

SQM Research, Property Gross Rental Yield - National

Real Estate Institute of WA, Strong property market conditions expected in WA in 2021

Did you find this page helpful?

Written by

Written by

Author

Adrian Edlington Commentary by

Commentary by

Guest Contributor

Bill TsouvalasPublished on August 19th, 2021

Last updated on March 19th, 2024

Fact checked

This guide provides general information and does not consider your individual needs, finances or objectives. We do not make any recommendation or suggestion about which product is best for you based on your specific situation and we do not compare all companies in the market, or all products offered by all companies. It’s always important to consider whether professional financial, legal or taxation advice is appropriate for you before choosing or purchasing a financial product.

The content on our website is produced by experts in the field of finance and reviewed as part of our editorial guidelines. We endeavour to keep all information across our site updated with accurate information.