How do personal loans work?

Personal loans work in the same way as any other standard loan product. When approved, you’re given a lump sum to be repaid with interest and fees over a set period of between one and seven years. This can be done in weekly, fortnightly or monthly instalments. You can apply for your loan online and have your application approved as soon as the same day in some cases.

With a personal loan, you can borrow from as little as $5,001 or as much as $75,000 (unsecured) or even $100,000 (secured). Amounts of $5,000 or lower fall under the small or medium loan category, which come with their own rules and regulations.

Personal loan interest rates

What is a good personal loan interest rate?

As of July 2026, the best personal loan interest rate available through Savvy is 6.49% p.a. However, the lowest rates are generally reserved for secured personal loans, for things like cars, and applicants with spotless financial profiles.

It’s important to understand that a good personal loan rate for you is specific to your situation. For example, someone with perfect credit and strong financials may be able to access a secured loan in the 7.00% p.a. to 8.00% p.a. range. If you're financing another asset, such as a caravan, bike or boat, you should be able to keep it under 10.00% p.a. If your financials aren't as strong, the rate may creep into the double digits.

Most unsecured personal loans are at least a couple of percentage points higher than their secured counterparts. For unsecured, while advertised rates might start with a 6 or 7, you're going to need to have a near-perfect credit score and be earning a high wage. If not, a good rate would be anything near 10.00% p.a., given there's no security.

These ranges are only examples and aren’t necessarily indicative of where you might land, but it’s important to illustrate that not everyone will have access to the lowest rates available. You can speak to your Savvy broker about what the best rates are for you right now.

What can you use a personal loan for?

There’s so much you can use a personal loan for. In most cases, you can use unsecured loans however you like, while secured loans may be restricted to the asset you’re buying (such as a caravan). Some providers don’t have these restrictions on their secured personal loans, though. Here are just a few of the things your loan can help you out with:

Debt consolidation

Having multiple debts on different schedules can be difficult to juggle, especially if they have high interest rates. Consolidate them into a single payment with a personal loan.

Home renovations

If you don’t want to eat into your savings to fund improvements to your home, a personal loan allows you to pay your tradies now and chip away at the overall cost at your speed.

Debt consolidation has jumped up to our most popular personal loan enquiry to start 2026 on the back of cost living pressures.

Medical expenses

They just have a habit of popping up at the worst times, don’t they? You can take out a loan to clear the expenses your health insurance doesn’t want to cover.

Weddings and honeymoons

As time goes on, weddings certainly aren’t getting any cheaper. If your dream ceremony is just out of reach financially, a loan could help you make it happen.

Travel and holidays

Whether you’re planning a months-long getaway to Europe or trekking around Australia in your caravan, applying for a loan helps you do it your way.

Legal fees

We all know lawyers are expensive. The more work involved, the greater the bill you’ll be up for. Customise your loan to suit your needs and maximise your comfort.

Asset finance

Whether you’re in the market for a new or used car, motorbike, caravan, jet ski or even a boat, you can take out a secured or unsecured loan to make your purchase goals a reality.

Why apply for a personal loan with Savvy?

How much interest will I have to pay on my loan?

There’s a lot that goes into determining your personal loan interest rate. First, here are some of the key variables that your lender will look at when determining your rate:

- Your credit score: the better your score, the lower your interest rate will be. Lenders reward applicants with positive credit histories.

- Your income: you’ll also likely benefit from lower rates the more comfortably you can cover your loan repayments.

- Your debts: lenders will consider the debts you're currently paying off and how you've managed them.

- Your employment: lenders look for stability in your job and pay. Maintaining the same job for an extended period can help you out.

- Your history repaying other loans: beyond your credit score, lenders value clear evidence that you can handle loan repayments. Successful personal loan repayments in the past go a long way.

- Whether it’s secured or unsecured: opting for a secured loan will bring with it a lower rate than an unsecured loan.

How bank statements can impact your personal loan rate

"If you’re taking out an unsecured personal loan, it’s mandatory for almost all lenders to want to see 90 days' worth of bank statements, as there’s no security on their end. It’s important to keep that in mind because if there were things like gambling, ATM transactions or dishonours in your statements, they could greatly impact your rate."

You can crunch the numbers yourself for different interest rates using our simple personal loan repayment calculator:

Personal Loan Repayment Calculator

It’s important to have an idea of what your loan might cost you overall before you apply. Fortunately, Savvy’s personal loan calculator is simple to use and lets you know how much your repayments could be.

Your estimated repayments

$98.62

| Total interest paid: | Total amount to pay: |

| $1233.43 | $5,143.99 |

Example #1: The importance of comparing interest rates

Harry is in the market for a personal loan to help him clear some of his medical bills. He gets to work comparing some of the available options on the market to see just how much he could save by finding the lowest rate for his $20,000 loan:

| Loan amount | Loan term | Interest rate | Monthly repayment | Total interest |

|---|---|---|---|---|

| $20,000 | Five years | 9.50% p.a. | $421 | $5,203 |

| $20,000 | Five years | 8.95% p.a. | $415 | $4,881 |

| $20,000 | Five years | 8.15% p.a. | $407 | $4,418 |

| $20,000 | Five years | 7.20% p.a. | $398 | $3,875 |

| Calculations are for illustrative purposes only. Interest rate may not be reflective of the rate you’re offered on your personal loan. | ||||

Even for a personal loan on the lower end of the scale, Harry would save over $500 by opting for the 7.20% p.a. rate compared to 8.15% p.a.

Example #2: Picking the right loan term

Edward wants to take out a $40,000 personal loan to cover the installation of a pool in his backyard. Although he knows how much he needs for the loan, he’s unsure which loan term is best for his situation. He runs the numbers on different loan terms and finds the following:

| Loan amount | Loan term | Interest rate | Monthly repayment | Total interest |

|---|---|---|---|---|

| $40,000 | Six years | 7.50% p.a. | $692 | $9,796 |

| $40,000 | Five years | 7.50% p.a. | $802 | $8,092 |

| $40,000 | Four years | 7.50% p.a. | $968 | $6,424 |

| $40,000 | Three years | 7.50% p.a. | $1,245 | $4,793 |

| Calculations are for illustrative purposes only. Interest rate may not be reflective of the rate you’re offered on your personal loan. | ||||

After considering what each option will cost overall, Edward decides to choose a four-year term, as he can still comfortably afford the higher monthly payment while minimising his interest bill.

Example #3: Deciding how much to borrow

Bonnie is saving up for her wedding, but knows she’ll need a loan to help her cover part of the cost. What she’s still considering is how much to pay out of pocket, as she wants to minimise the interest she’ll have to pay while not depleting her savings. She runs the calculations based on a five-year loan term at 6.95% p.a. and produces the following table:

| Loan amount | Loan term | Interest rate | Monthly repayment | Total interest |

|---|---|---|---|---|

| $30,000 | Five years | 6.95% p.a. | $594 | $5,600 |

| $35,000 | Five years | 6.95% p.a. | $693 | $6,533 |

| $40,000 | Five years | 6.95% p.a. | $792 | $7,467 |

| $45,000 | Five years | 6.95% p.a. | $890 | $8,400 |

| $50,000 | Five years | 6.95% p.a. | $989 | $9,333 |

| Calculations are for illustrative purposes only. Interest rate may not be reflective of the rate you’re offered on your personal loan. | ||||

She sees that with every extra $5,000 she borrows, her interest bill increases by over $900 and her monthly payments go up by almost $100. She decides that the best balance between her bank balance and interest savings is the $35,000 loan.

Personal loan pros and cons

Pros

-

Use them how you like

Personal loans are (mostly) unsecured and highly flexible. You can use them for just about anything you like, including multiple purposes within the same loan.

-

Tailor your repayments to your needs

You’ll be able to choose the loan term and payment schedule that suits your requirements, down to optional additional repayments.

-

Fast online application and approval

One key benefit of personal loans is their speed. Some lenders can turn applications around and have them approved on the same day you apply.

Cons

-

Higher interest and fees

Personal loans tend to come with more expensive rates and fees than other loan types, so they may cost you more overall.

-

Potentially lower borrowing caps

While car loans sometimes have no upper limit, unsecured personal loans aren’t available for more than $75,000 (some lenders set this limit at $50,000).

How to apply for your personal loan online with Savvy

-

Apply online

Complete our simple form by telling us about yourself.

-

Send through your docs

We may need additional info to verify your application.

-

Speak to your Savvy broker

We’ll give you a call to talk through your personal loan options.

-

Have your application prepared

Your broker will prepare and submit your application to your lender.

-

Get approved and settled

Once approved, we’ll handle loan settlement and the funds will be yours!

Personal loan statistics: 2025

The average personal loan amount requested through Savvy’s online application process in 2025 was $27,238.

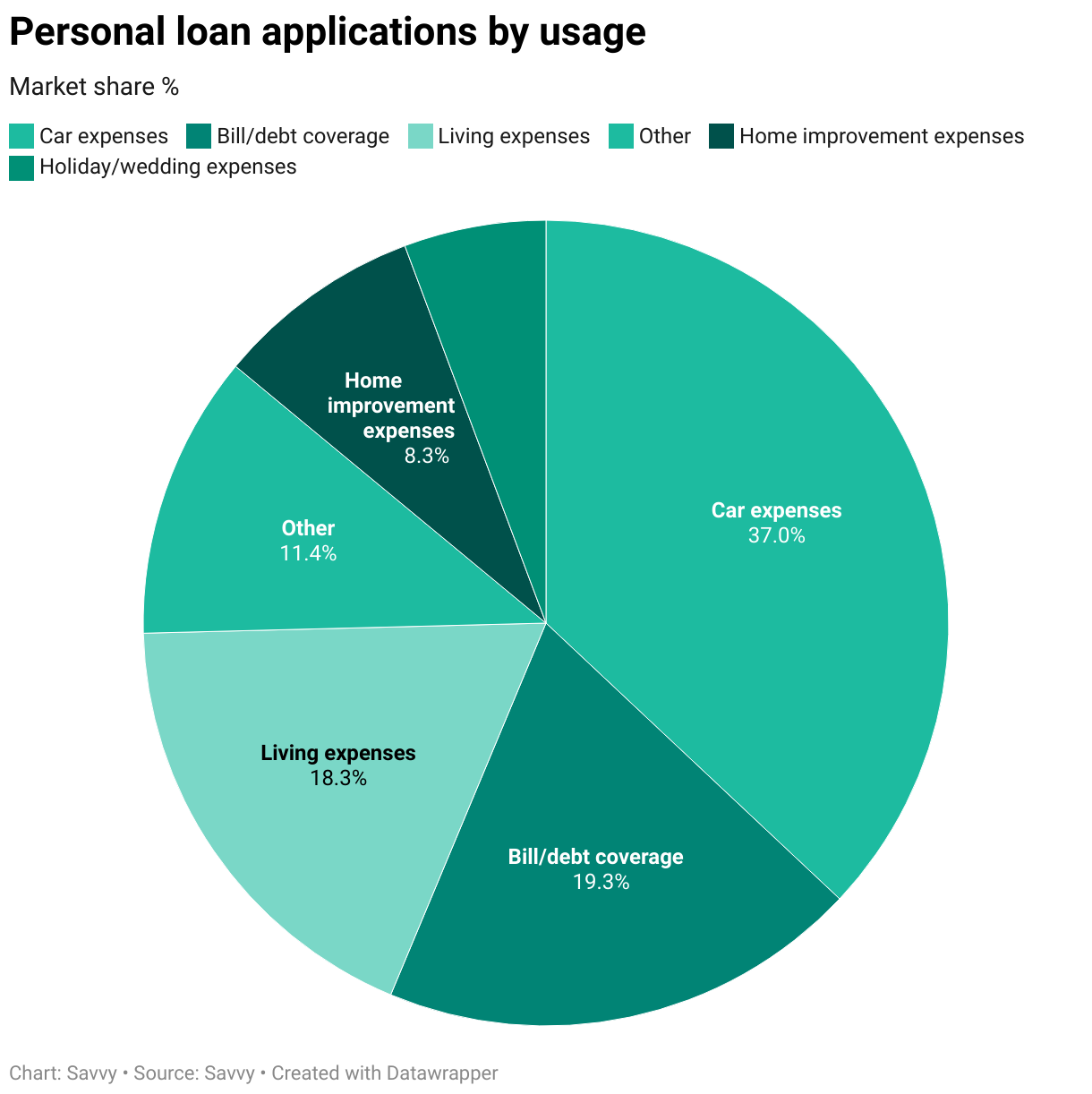

When it comes to the most common uses of personal loans, though, there are a few standout reasons for borrowing. Across the 2025 calendar year, the most common reasons cited for applying for a personal loan were car expenses (37.6%), recreational vehicle expenses (18.0%) and bill or debt coverage (8.3%).

It’s clear that personal loans are a rapidly growing market in Australia. According to the Australian Bureau of Statistics (ABS), the seasonally adjusted value of new personal fixed term loan commitments (road vehicle purchases excluded) has continued to rise since the June Quarter of 2020.

This value peaked at $9.307 billion in the September Quarter of 2025, with loans for the purchase of road vehicles ($4.919 billion) and other purposes, including personal investment, travel and holidays, other vehicles and household goods ($4.450 billion combined) also reaching all-time highs.

The June Quarter of 2025 also saw a 11.6% uptick in personal loan applications compared to the same period last year, according to Equifax.

Key tips for comparing personal loans

-

Look at the comparison rate and read the fine print

Advertised interest rates only tell half the story. The loan’s comparison rates provide a more accurate indication of the true cost, inclusive of fees. If there are any fees hidden in the fine print, you’ll need to know about them before you sign.

-

Prioritise flexibility in your repayments

Most personal loans will allow you to make free additional repayments, but not all offer this. Having this option leaves the door open for potential savings.

-

Make sure you’re eligible before you apply

There’s no use wasting time on lenders whose criteria you fail to meet. For example, applying with a lender whose income threshold is higher than what you earn or only accepts customers above a certain credit score could result in an instant rejection. When you apply with Savvy, we’ll only match you with lenders available to you.

-

Take the time to consider which option is best

Rushing into things could cost you in the long run. By comparing all your finance and lender options (or having someone like us do it for you), you can be more confident in your decision.