What are car loans and how do they work?

A car loan is a product designed to help borrowers purchase a new or used vehicle. They’re typically repaid over a period of one to seven years, which you’ll often have a say in when you apply. A lender, after conducting responsible lending checks, will approve a loan if the applicant meets their eligibility criteria. This loan is then transferred directly to their dealer or seller. In return, the borrower must pay back their lender in set instalments with interest and fees.

Compare car loan interest rates

We've taken a snapshot of the 12 cheapest rates currently on offer in the Savvy database. Keep in mind that the interest rate you'll receive will vary depending on your credit score and other factors. The comparison rate shown is the true rate you'll pay, as it includes monthly and establishment fees charged by the lender.

As of May 2026, the cheapest new car loan interest rates available through Savvy's partnered lenders are as follows:

The average car loan interest rate among those currently available through Savvy is 7.58% p.a. for borrowers with good credit.

Getting the best car loan deal

"Many people focus on getting the lowest interest rate, but that’s only half the story. A loan with fewer fees, flexible repayment options or no early exit penalties can often save you more in the long run. Don’t just ask ‘what’s the rate?’; find out what the total cost of the car loan will be over its life."

The types of car loan interest rates

Car loans typically come with fixed interest rates, which remain locked in throughout your term. This makes them better for budgeting into the future, as you’re protected against rate rises across your term and will pay the same each week, fortnight or month. However, some lenders may allow you to choose variable rates, which can change from month to month. This means you can benefit if rates fall, but will have to pay more if they go up.

Other factors impacting your car loan interest rate

Additionally, the rate you’re offered on your loan will depend on several different personal variables, such as:

- Your job and income stability

- Your credit score and history

- Your savings

- Your assets and liabilities

- The type of car you purchase and its condition, including whether it's electric or hybrid

- Your dependants (if you have any)

Types of car loans

Pros and cons of car loans

Pros

-

Immediate car ownership

As long as you're approved, a car loan can get you into a brand-new vehicle in as little as a few days. So, whether you’re upgrading or purchasing your first car, you can make it happen sooner.

-

Keep your savings intact

Instead of needing to take from your savings to pay for a car, you can finance the entire purchase price of the vehicle with your loan.

-

Flexible loan options

You can take out a car loan for up to seven years in length. You also get to pick the repayment frequency, which allows you to tailor your instalments to fit your budget.

Cons

-

Interest repayments

Unfortunately, all loans attract interest. While it does make the upfront cost of the car far cheaper, you’ll pay more than the lifetime value of the car in the long run.

-

Affects your borrowing capacity

If you’re planning to take out another loan while you’re still paying off your car finance deal, your borrowing capacity will be reduced due to the increased debt-to-income ratio.

-

Vehicle eligibility

Cars that are approaching 15 years old by the end of the loan term may have a smaller pool of lenders willing to finance them. This could mean your only option with many lenders is an unsecured loan, which is usually more expensive.

Why apply for a car loan with Savvy?

Cheap car loan rates

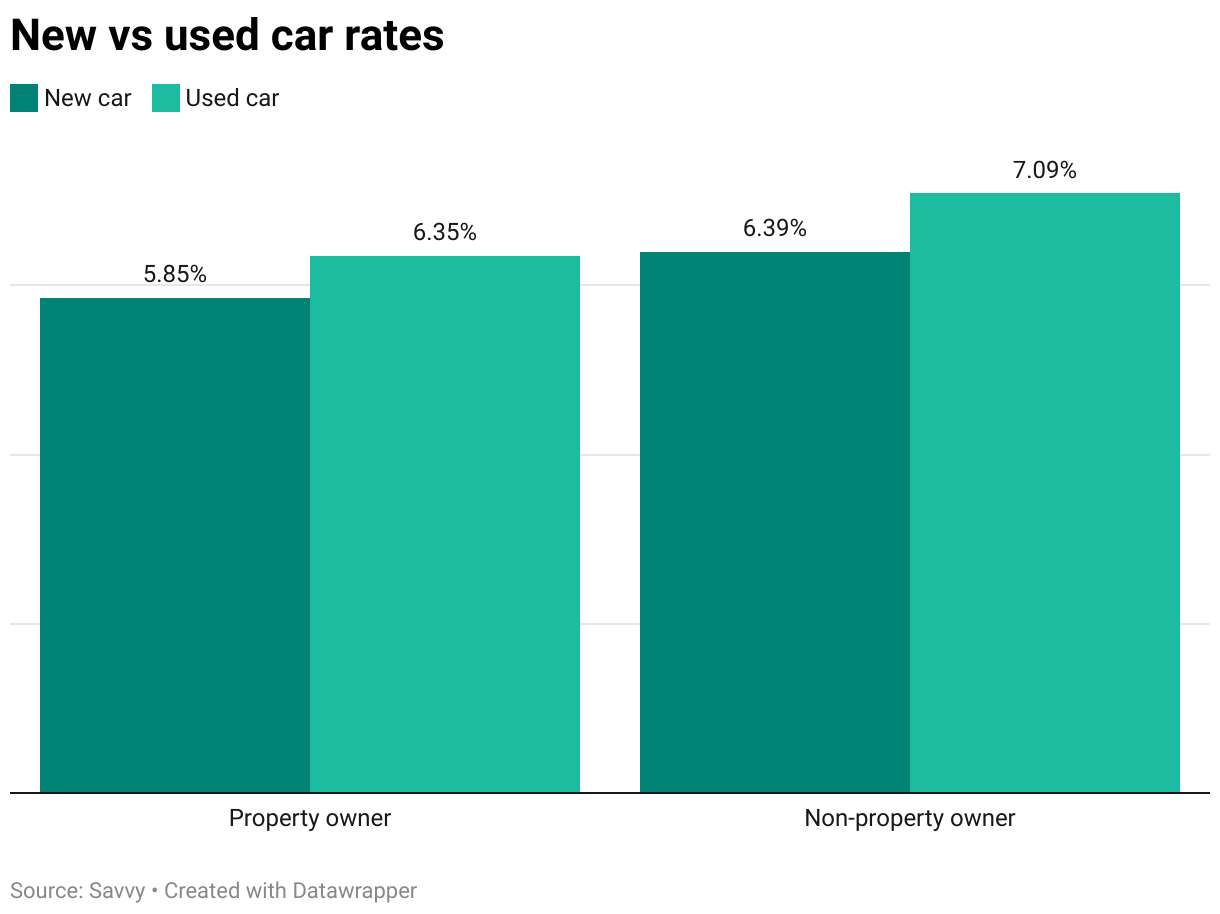

As of April 2026, the cheapest car loan rate on offer through Savvy is now 6.20% p.a. (7.87% p.a. comparison) with MoneyMe. The lender with the best car finance comparison rate is RACV at 7.37% p.a. (6.59% p.a. interest). However, that rate is for new car loans only.

Rates are slightly higher for older vehicles. If you’re buying a used car, the lowest rate available through Savvy is 6.48% p.a. (7.74% p.a. comparison). More than four out of five approved loans through us in 2025 (82.3%) were for used models from 2024 or earlier.

It isn’t just vehicle age that might affect your car loan rate, though. While the rates above are for property owners, the lowest available new car loan rate for renters is 6.39% p.a. (7.80% p.a. comparison). Almost two thirds of all approved car loans through Savvy in 2025 (66.2%) were for renters and boarders.

Some of the other key variables that can impact your interest rate are:

- Fixed vs variable: as mentioned, fixed rates are far and away the most common on car loans. However, opting for a variable rate could mean you’re paying more now but less in the long run if rates continue to fall.

- Your employment: applicants who have a consistent employment history and receive a stable income will often receive lower rates than those with frequent job changes or inconsistent hours.

- Your credit score: this is probably the number one factor when it comes to setting your interest rate. If you’ve had credit issues that are still listed on your file, your interest rate is likely to be much higher. The average credit score of customers who took out a new car loan through Savvy was 769 in the last year.

- Your current debt-to-income ratio: if lenders feel that the debt you’re currently paying off is too great a percentage of your total pay, your rate will be increased or your application will be rejected.

What will your car loan repayments look like?

What your car loan repayments end up looking like is determined by a wide range of factors specific to you, your lender and the car you're buying. Perhaps the most significant is the model of car you've chosen and whether it's new or used.

We’ve put together a cost comparison for the top-of-the-line models for the most popular utes, SUVs and sedans in Australia (based on VFACTS data), both new and used, to show how they differ in total cost over a five-year loan term.

When you think of a car loan, you might automatically assume a new vehicle, but 65.1% of cars sold in Australia in 2025 were used.

Most popular cars in Australia and what they'll cost you

MG ZS Excite 2WD

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2023 | $17,990 | 6.48% p.a. | $352 | $3,120 |

| 2026 | $22,990 | 5.50% p.a. | $440 | $3,359 |

|

2023 2026 |

|

$17,990 $22,990 |

|

6.48% p.a. 5.50% p.a. |

|

$352 $440 |

|

$3,120 $3,359 |

Toyota Corolla Sedan ZR HEV

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2023 | $38,990 | 6.48% p.a. | $763 | $6,762 |

| 2026 | $40,260 | 5.50% p.a. | $770 | $5,881 |

|

2023 2026 |

|

$38,990 $40,260 |

|

6.48% p.a. 5.50% p.a. |

|

$763 $770 |

|

$6,762 $5,881 |

Toyota RAV4 Edge AWD Hybrid

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2023 | $55,000 | 6.48% p.a. | $1,076 | $9,538 |

| 2026 | $58,360 | 5.50% p.a. | $1,115 | $8,525 |

|

2023 2026 |

|

$55,000 $58,360 |

|

6.48% p.a. 5.50% p.a. |

|

$1,076 $1,115 |

|

$9,538 $8,525 |

Ford Ranger Raptor 3.0 4X4

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2023.5 | $79,990 | 6.48% p.a. | $1,565 | $13,871 |

| 2026 | $90,690 | 5.50% p.a. | $1,733 | $13,248 |

|

2023.5 2026 |

|

$79,990 $90,690 |

|

6.48% p.a. 5.50% p.a. |

|

$1,565 $1,733 |

|

$13,871 $13,248 |

Mercedes-Benz EQE 350 4MATIC Sedan

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2023 | $99,000 | 6.48% p.a. | $1,937 | $17,168 |

| 2026 | $155,400 | 5.50% p.a. | $2,969 | $22,700 |

|

2023 2026 |

|

$99,000 $155,400 |

|

6.48% p.a. 5.50% p.a. |

|

$1,937 $2,969 |

|

$17,168 $22,700 |

Calculations are for illustrative purposes only and do not include other car-buying costs. Model costs obtained through CarsGuide. Used car costs are examples based on listings obtained from carsales from August 2025. All figures are rounded up to the nearest dollar. Interest rates are reflective of the minimum available rate for each car age as of August 2025. The rate you receive on your car loan may be different to the rates listed above.

As you can see here, the cheapest finance option isn’t always necessarily the used car. It often depends on the interest rate you’re offered on your car loan. The average car loan in Australia is $36,000, meaning that over a five-year term, the average monthly repayment is $759. That’s in line with the monthly repayments of a 2026 top-of-the-line Toyota Corolla sedan as shown above.

Another factor to consider if you want a lower car repayment is a residual or balloon payment. This decreases your monthly repayments but increases your overall interest. For example, on a $40,000 car loan, you could save around $160 each month with a 30% balloon, but you'd pay close to $2,400 over the life of the loan.

If you’re looking to crunch the numbers on car loans yourself, you can use Savvy’s handy car loan repayment calculator to see how different loans, terms and rates impact your repayments.

Car Loan Repayment Calculator

Your estimated repayments

$98.62

| Total interest paid: | Total amount to pay: |

| $1233.43 | $5,143.99 |

How much could you borrow for a car loan?

Just because you need a new car doesn’t mean the bank will automatically hand out the money. Your individual borrowing power determines the size of loan you can be approved for. It must be manageable for you to pay off in weekly, fortnightly or monthly instalments.

Lenders will base your borrowing power on things like your income, employment, outstanding debts, credit history and the number of dependants you have. The following tables show how some of these variables can impact how much you can borrow:

Co-applicant borrowing capacity

| Income | 0 dependants | 1 dependant | 2 dependants |

|---|---|---|---|

| $80,000 | $26,782 | N/A | N/A |

| $90,000 | $63,918 | $37,563 | $19,120 |

| $100,000 | $101,053 | $74,698 | $56,255 |

| $110,000 | $114,590 | $99,476 | $81,245 |

| $120,000 | $150,000 | $125,143 | $106,912 |

| $130,000 | $150,000 | $150,000 | $138,374 |

| $140,000 | $150,000 | $150,000 | $150,000 |

| Note: rates are calculated based on a $30,000, five-year car loan for a new vehicle bought by an asset-backed applicant. | |||

Your borrowing power can drop for reasons you might not expect, like credit cards or HELP debts. Even with no balance, a card’s limit still counts. For example, a couple earning $100,000 with one dependant would see their borrowing capacity fall from $74,698 to $53,552 just by having a $10,000 credit card limit.

Single applicant borrowing capacity

| Income | 0 dependants | 1 dependant | 2 dependants |

|---|---|---|---|

| $60,000 | $18,855 | N/A | N/A |

| $70,000 | $35,919 | $16,061 | N/A |

| $80,000 | $64,646 | $35,019 | N/A |

| $90,000 | $101,782 | $72,155 | $41,149 |

| $100,000 | $138,917 | $109,290 | $78,284 |

| $110,000 | $150,000 | $122,830 | $91,783 |

| $120,000 | $150,000 | $150,000 | $128,918 |

| Note: rates are calculated based on a $30,000, five-year car loan for a new vehicle bought by an asset-backed applicant. | |||

Budgeting for your car loan

"Once you add your partner into the mix, your borrowing capacity becomes less straightforward if their name isn’t going on the loan. Even if you’re living in a sharehouse where not everyone’s names are on the lease, a lender can wipe thousands off your borrowing capacity. Checking what you can comfortably afford before applying (especially with a dealership or lender) allows you to find a car in your budget and avoid being rejected."

How to apply for your car loan with Savvy

-

Apply online

Complete our simple online form.

-

Submit documents

For verifying your personal info.

-

Chat to your broker

Speak about your car finance options on the phone. This is where you can be pre-approved.

-

Find your car

Through our in-house car broker (if you haven't already).

-

Get approved

Have your application prepared and greenlit.

-

Signed, sealed, delivered

We'll handle settlement and you can drive away!

Do I qualify for a car loan?

Every lender has their own eligibility criteria for car loans, so this can vary depending on who you apply with. However, these are the standard points you'll need to meet:

-

Age

You must be at least 18 years of age.

-

Residency

You must be an Australian citizen or permanent resident (or, in some cases, an eligible visa holder).

-

Income

You must be earning a stable income that is enough to comfortably support your repayments. Some of the lenders we work with state that this can start from as little as $480 per week and include certain Centrelink benefits.

-

Employment

You must be employed and earning a consistent income from your job.

-

Credit score

You must meet your lender’s requirements related to your credit score.

-

Car

Your car must meet your lender’s requirements related to type, age and condition.

New car loans vs used car loans

When it comes to choosing the right vehicle for your needs, one question might be sticking out above the rest: should I buy new or used? There are several important differences between loans for brand-new cars and those for pre-owned models:

- Size of the loan: of course, you can expect to pay more for a new car. Brand-new models can lose up to 30% of their value in the first year. In 2025, the average new car loan was $52,332, compared to $34,529 for used cars. As a result, you’re less likely to end up with significant negative equity on a used car.

- Interest rate: new cars will often have lower rates than used cars, which can save you on interest overall. In 2025, the average new car interest rate through Savvy was 9.58% p.a., while the average used car rate was 13.07% p.a.

- Stock availability: if you want to get into your ride sooner, used models might be the way to go. While new vehicles often have to be shipped in and are subject to waitlists with dealerships, buying used through a dealer or private seller usually means the car is available for you to buy straight away.

- Age limits: although all lenders will finance used cars, that’ll only be up to a point. Some will cap the maximum age of financed vehicles at ten years by the end of your loan, while others extend this to 15 or 20 (and sometimes more). If your car is going to be ten years or older by the end of your term, you might not have as many options to choose from.