How do chattel mortgages work?

Chattel mortgages work in a very similar way to a standard car loan, with several areas tailored to commercial needs. Here’s how they work:

- Buy new or used (provided it meets your lender’s criteria)

- Borrow from $5,001, with many lenders not having a set borrowing limit (though usually up to $250,000 for low doc applicants)

- Have your loan secured by your asset (as collateral)

- Repay your loan over between one and seven years

- Make payments on a weekly, fortnightly or monthly schedule

- Repay with interest and fees (some may waive certain fees)

- Deposits and balloon/residual payments are optional

- Early repayments may be available with some lenders

Chattel mortgage tax benefits

The biggest difference between chattel mortgages and car loans is their tax benefits. Under a chattel mortgage agreement, you can claim the following:

- Interest on your loan repayments

- GST on the purchase of the asset

- Depreciation of the asset over time

It’s important to note that you’ll only be able to claim the business portion of each of these expenses. For example, if you’re using your business’ car for commercial purposes 75% of the time, you can claim up to 75% of the above expenses back on tax. You can only claim the full amount if your asset isn’t used for personal purposes at all.

If you’re unsure how much to claim, you should speak to your accountant or a tax professional. Every business is different, so it’s crucial to get personalised advice before you complete your tax return.

Chattel mortgage interest rates

Commercial loan interest rates are usually higher than secured consumer finance, such as car loans. As of September 2025, the lowest available chattel mortgage rates available through Savvy are:

However, lenders set commercial loan rates based on a variety of factors specific to you and your business. These can include:

- Your business’ credit score (and yours): a business with a strong credit record is likely to receive a rate on the lower end of the scale. Your personal score will also be included in the equation.

- Your personal assets: if you’re asset-backed (meaning you own your home), your business may qualify for a reduced rate.

- Your business’ revenue and expenses: lenders look at your business’ incomings and outgoings when assessing your application. The more profitable, the better.

- Your business’ assets and liabilities: any existing commercial assets owned by your business will be factored in, as will outstanding debts like other loans.

- Your business’ trading history: a relatively new company with only a few months in business will be charged a higher rate than one with an extensive trading history and proven track record.

- The asset you buy: a car won’t attract the same interest rate as a piece of equipment. Specialised commercial assets usually come with higher rates than road vehicles.

How are chattel mortgages different to leases?

There are several key differences between chattel mortgages and finance or operating leases. Let’s break it down:

| Chattel mortgage | Commercial lease | |

|---|---|---|

| Ownership? | From the start | Optional at the end of the agreement |

| Tax-deductible payments? | Interest only | Yes (subject to usage) |

| Residual included? | Optional | Mandatory |

| Options at the end of the agreement? | Whatever you like, as you’ll own the asset | Buy, sell or trade in the asset or refinance the residual to continue your lease (finance lease) Hand back the asset to your lessor (operating lease) |

| Available terms? | 1 to 7 years | 1 to 5 years (up to 7 is possible if the residual is refinanced) |

| Ability to use a deposit/trade-in? | Yes | No |

| Common uses: | Purchase of commercial road vehicles, as well as valuable equipment | Heavy machinery and vehicles that require refreshing, such as tech equipment |

Chattel mortgages vs novated leases

A novated lease is different from a commercial lease. It’s designed for salaried employees buying a car and involves having their lease payments deducted from their pre-tax income (known as salary sacrificing).

The benefit here is that your taxable income is reduced, which can save a substantial amount in income tax overall. The GST on the purchase of your car can also be claimed, while lease providers can access competitive fleet discounts.

Because a salary is required to run a novated lease, you won’t be able to get one if you don’t pay yourself a consistent wage. Although they can be used for commercial purposes, it’s uncommon for this to be the case. All in all, novated leases are unlikely to be the best option for most business owners in this situation.

Chattel mortgages vs hire purchases

Hire purchases are another type of commercial arrangement. This involves a provider purchasing an asset and hiring it out to a business. That business pays for it in instalments and eventually, after the final payment is made, has ownership of the asset transferred to it.

These were popular with businesses looking to take advantage of off-balance sheet accounting, as they don’t initially own the asset. However, chattel mortgages and leases are the predominant finance type in today’s market.

Chattel mortgage repayment calculator

As you can see by using the chattel mortgage calculator, there are plenty of factors that can impact the cost of your loan deal. The following table shows how much the loan term you choose affects your repayments and interest:

| Loan amount | Loan term | Interest rate | Monthly repayment | Total interest |

|---|---|---|---|---|

| $50,000 | Four years | 7.50% p.a. | $1,202 | $7,669 |

| $50,000 | Five years | 7.50% p.a. | $966 | $9,741 |

| $50,000 | Six years | 7.50% p.a. | $860 | $11,858 |

| $50,000 | Seven years | 7.50% p.a. | $763 | $14,021 |

| Calculations are for illustrative purposes only. Interest rate based on average rate available through Savvy in the 2024-25 financial year. | ||||

Another factor to consider here is the balloon payment. While these are compulsory for finance and novated leases, they’re optional for chattel mortgages. Adding a balloon will reduce your monthly repayments, but increase the total interest you’ll pay, as the following table demonstrates:

| Loan amount | Loan term | Balloon payment | Interest rate | Monthly repayment | Total interest |

|---|---|---|---|---|---|

| $100,000 | Five years | $5,000 | 7.50% p.a. | $1,923 | $20,371 |

| $100,000 | Five years | $10,000 | 7.50% p.a. | $1,855 | $21,260 |

| $100,000 | Five years | $20,000 | 7.50% p.a. | $1,718 | $23,039 |

| $100,000 | Five years | $35,000 | 7.50% p.a. | $722 | $13,298 |

| Calculations are for illustrative purposes only. Interest rate based on average rate available through Savvy in the 2024-25 financial year. | |||||

The power of the balloon

"Balloons are common practice for business owners, especially those who look to update their vehicle every two to three years. A good broker can tailor your balloon payment to fit your preferred budget."

Why apply for a business loan with Savvy?

Chattel mortgage pros and cons

Pros

-

Borrow up to 100% of your asset’s price

A chattel mortgage allows you to buy your asset without eating into your business’ cash reserves, with high maximum loan amounts available from lenders.

-

Own your vehicle or equipment from the start

Your business will own the asset from the start, so you’ll have more freedom to use it how you like (certain modifications may not be allowed, though).

-

Enjoy tax benefits

Perhaps the biggest advantage from a financial perspective is the ability to claim part or all of your loan’s expenses on tax, in addition to GST and depreciation.

-

Add a customisable deposit or residual

You can pay a deposit upfront, a balloon at the end of your term or both to reduce your payments. Unlike leases, chattel mortgage residuals are customisable.

Cons

-

Early repayment fees may apply

If you decide you want to clear your loan ahead of schedule, you could be slugged with steep early termination fees by your lender.

-

Assets must meet lender requirements

You can’t just buy any old car or equipment. Because the loan is secured, it’ll need to be accepted by your lender, including falling within its age and condition criteria.

-

Can only be used for a single asset purchase

Chattel mortgages are designed solely for the purchase of the asset you’re buying. You may be able to include on-road costs like insurance, registration and vehicle duty, though.

How to apply for a chattel mortgage with Savvy

-

Apply online

Fill out the short form on our site and tell us what you’re after.

-

Submit your documents

We may need docs to verify your profile. You can submit them online.

-

Chat with your Savvy finance broker

We’ll give you a call to discuss your commercial finance options.

-

Find your car (if you’re buying one)

We can help you source your vehicle at a competitive price.

-

Have your application prepared

Your broker submits your application for formal assessment.

-

Get approval and sign off

Once you’re approved, all that’s left is to sign off and secure your asset!

Chattel mortgage statistics: 2024-25

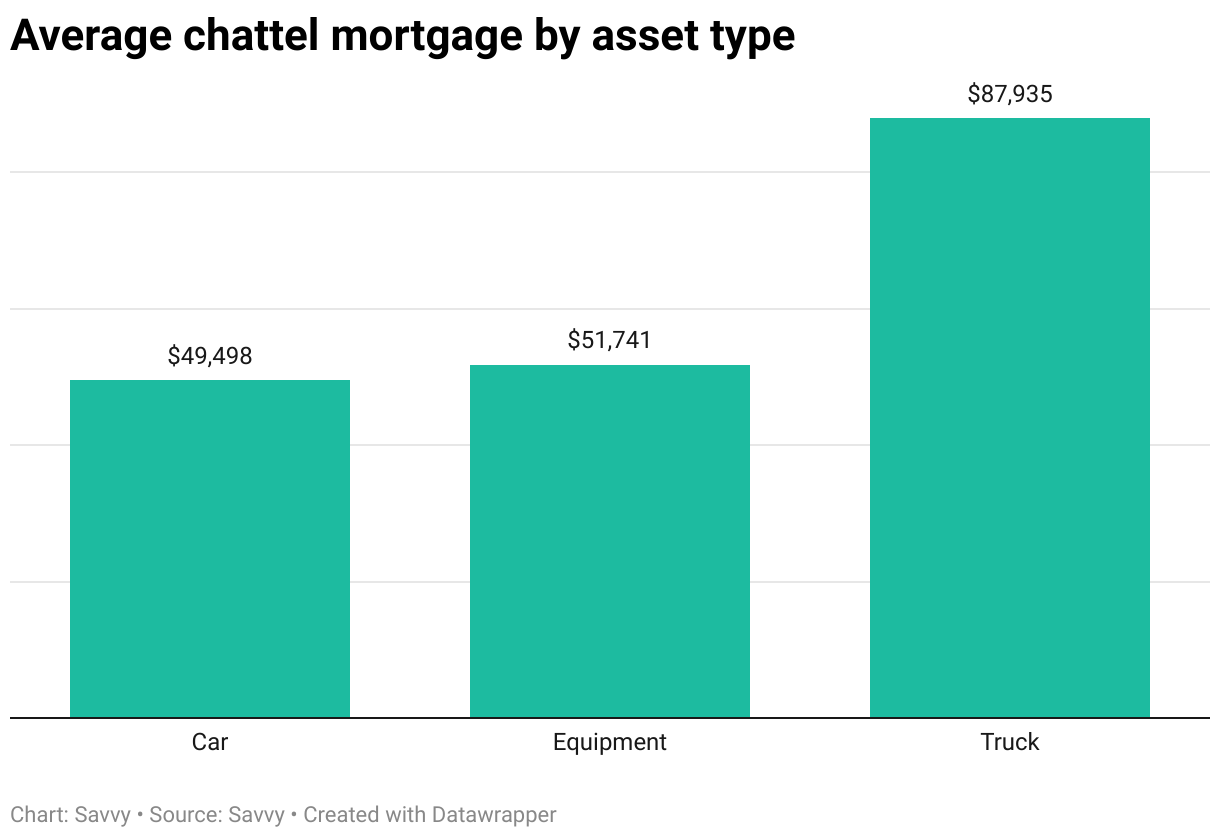

Across the 2024-25 financial year, the average chattel mortgage taken out through Savvy was $51,870 across a five-year loan term. This number is made up of commercial car, equipment and truck finance deals.

However, when you split them apart, you can see how much business owners are borrowing to purchase each asset on average:

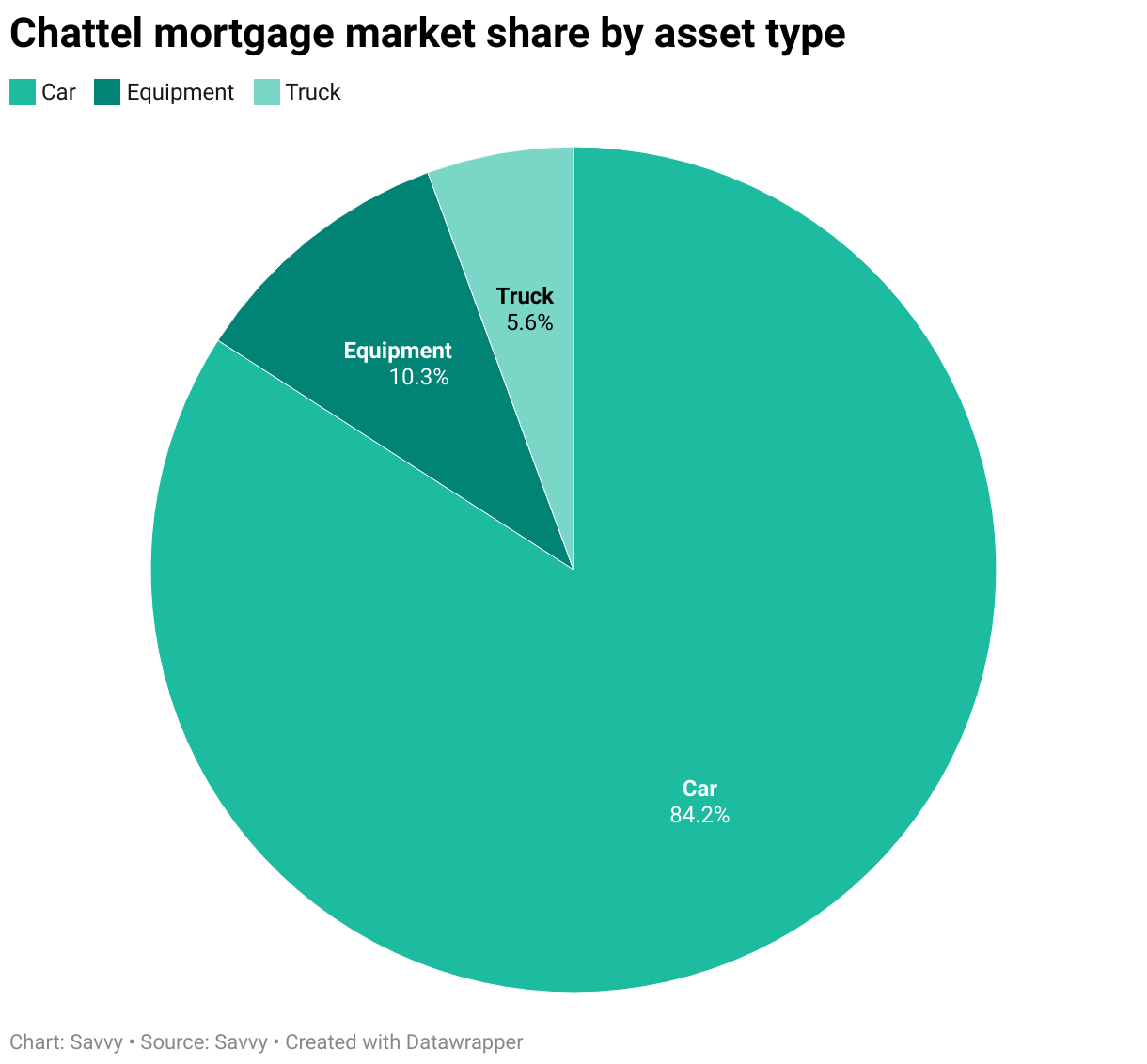

As you can see, the average chattel mortgage falls far closer to the average car and equipment loan amount than the average truck loan sum. That’s because cars were far and away the most popular. They accounted for almost 85% of all commercial asset finance approved through Savvy over that period.

In contrast, one in every ten deals was for a piece of equipment, while one in every 20 was a truck. Because of their increased value, though, trucks made up just under 10% of the total value of commercial asset finance.

While vehicle sales as a whole have dipped in Australia compared to last year’s numbers, light commercial vehicle sales have remained relatively consistent, according to the Federal Chamber of Automotive Industries (FCAI). The segment is just 1.3% behind last year’s sales to this point, compared to an overall decline of 2.7% across all segments, while its July performance is a 3.3% improvement on the same period last year.

Heavy commercial vehicles, on the other hand, have had a tougher year in sales. Their total year-to-date sales are 11.2% lower so far this year than last, while their July numbers are 6.6% lower. The reason for this, according to the CEO of Truck Industry Council (TIC), Tony McMullan, is at least partly attributable to May’s federal election.

New commercial vehicle sales: July 2025

| Category | August 2025 | August 2024 | % change vs 2024 | YTD 2025 | YTD 2024 | % change vs 2024 |

|---|---|---|---|---|---|---|

| Light commercial | 23,211 | 22,507 | 3.1% | 184,948 | 186,307 | -0.7% |

| Heavy commercial | 3,630 | 4,114 | -11.8% | 29,909 | 33,691 | -11.2% |

| Total market | 26,841 | 26,621 | 0.8% | 214,857 | 219,998 | -2.3% |

| Source: New Vehicle Sales: August 2025, Federal Chamber of Automotive Industries | ||||||

“Historically new heavy vehicle sales have always slowed in the run-up to a federal election, with businesses potentially waiting to witness the market reaction to the election result before committing to fleet replacements and/or business expansion,” said McMullan.

“With the election result now known and with the Labor Government returned, Australian businesses have a reasonable insight into the economic environment for the next three years.”