Business equipment finance rates

There are several ways to finance equipment depending on your needs. The rates below are for commercial equipment loans and reflect the lowest rates available through Savvy as of July 2026.

Rates are indicative only and based on a business with an ABN registered for at least eight years, GST registration for at least four years, a 60-month loan term and a $50,000 purchase. Your actual interest rate will depend on factors including your business profile, credit history, financial position, the equipment being financed, loan amount, term and the lender's assessment criteria.

Types of equipment finance

When financing equipment for your business, you can choose between a loan or a lease depending on how you want to use the asset and whether you want ownership.

These are your main options:

Equipment loan (chattel mortgage)

With a chattel mortgage, a lender provides the funds to purchase your equipment, with the asset used as security for the loan. You have immediate ownership and control of the equipment, and you repay the loan over a set term, usually between one and seven years. Because the loan is secured, the lender may repossess the equipment if repayments are not met.

Finance lease

Under a finance lease, the lender purchases the equipment and leases it to your business for a fixed term, usually one to five years. You make regular payments to use the asset, but the lender retains ownership during the lease period. You are typically responsible for maintenance and running costs. At the end of the term, you may have the option to purchase the equipment, extend the lease, or upgrade to a new asset.

Operating lease

An operating lease is a shorter-term rental arrangement where you use the equipment without taking ownership. You pay to use the asset for a set period, and the lessor usually covers maintenance and servicing. Once the lease ends, you return the equipment with no ongoing obligation, making it suitable for assets that may need regular upgrading.

This is how the different types of finance compare:

| Feature | Chattel mortgage | Finance lease | Operating lease |

|---|---|---|---|

| Ownership | You own the equipment from day one | Lender owns the equipment during term | Lender owns the equipment throughout |

| Deposit | Optional – not required but can reduce repayments | No | No |

| Repayments | Fixed loan repayments | Fixed lease payments | Fixed lease payments |

| Balloon/residual option | Optional balloon payment | Mandatory residual payment | No |

| Maintenance responsibility | Your business | Your business | Usually the lessor |

| Flexibility | Less flexible – difficult to upgrade | Can upgrade at end of term | Easy to upgrade or switch |

| Customisation | Equipment can be modified | Typically no modifications allowed | No modifications allowed |

| Tax treatment | Interest and depreciation may be tax-deductible | Lease payments may be tax-deductible

GST claimable monthly |

Lease payments may be tax-deductible

GST claimable monthly |

These figures are for illustrative purposes only. Actual costs will vary depending on your business profile, the equipment you choose and the terms of your agreement. To understand your actual costs, it’s best to get a tailored quote.

Which type of finance should I choose?

The best choice between an equipment loan and lease comes down to how you use the asset and what matters most to your business. If you’re investing in long-lasting machinery that holds value and is central to your operations, a loan may be the better fit, allowing you to build equity and have full control over the equipment.

On the other hand, if you need flexibility or work in an industry where technology changes quickly, a lease can make more sense. Leasing is also useful for businesses that need short-term access to specialised equipment without committing to long-term ownership.

For example, a construction company buying an excavator they plan to use for years might benefit from a loan, while a medical practice upgrading diagnostic equipment every few years could find a lease more cost-effective.

Finance that fits your equipment

"Machinery and heavy equipment usually have longer lifespans, so lenders often offer longer finance terms. However, the best finance product depends on your business situation. Most of the time, a loan is suitable, but if you have a fleet of equipment or vehicles, a lease may be the better option."

What kind of equipment can I finance?

You can finance a wide range of new or used equipment for your business, whether it’s for daily operations, upgrades or specialist work.

Primary equipment

Vehicles and machinery used for core business activities like transport, construction, agriculture and trade.

- Vehicles: cars, vans, utes, motorbikes, trucks, trailers, buses

- Yellow goods: bulldozers, cranes, excavators, tractors, harvesters and other agricultural equipment

Secondary equipment

Industry-specific equipment used in production, services and commercial environments.

- Industrial and manufacturing plant

- Medical and healthcare equipment

- Restaurant and food manufacturing equipment

- Printing machinery

- Trade tools

- Mezzanine finance

Tertiary equipment

Technology and infrastructure that support day-to-day operations.

- IT hardware and software

- Telephony and communications

- Office fit-outs, furniture and equipment

- Gym and fitness equipment

- Solar systems

- POS systems

How much will my equipment finance cost?

The cost of equipment finance varies significantly depending on the type of finance you choose and the asset you’re buying. There’s no typical figure that applies across the board because equipment types, prices and rates differ so much. To give you an idea, here are some example scenarios showing hypothetical costs for a used Bobcat, new computer equipment and a heavy-duty crane across different finance options:

| Chattel mortgage | Finance lease | Operating lease | |

|---|---|---|---|

| Equipment | Bobcat skid-steer (used) | 50 MacBooks + 50 Dell monitors (new) | Tadano crane |

| Equipment cost | $50,000 | $125,000 | $500,000 |

| Loan/lease term | 5 years | 5 years | 5 years |

| Interest/lease rate | 12.5% p.a. | 8% p.a. | Bundled monthly rate |

| Balloon/residual | – | $35,162.50 (28.13%) | – |

| Monthly payment | $1,023 | $1,822 | $8,750 |

| Total cost | $61,359 | $144,498 | $525,000 |

| Ownership | Yes | Optional (after residual) | No |

When thinking about equipment finance, it’s important to look beyond just the repayments and focus on the return on investment (ROI) – the value your equipment delivers compared to what it costs to finance, operate and maintain. For instance, buying a Bobcat that you use regularly can save you money on short-term hire and allow you to complete more jobs, boosting your income. But if it sits idle most of the time, you’re paying off a depreciating asset instead of generating returns, turning it into an ongoing cost.

What influences the cost of equipment finance?

-

Interest rate

The interest rate is usually the biggest factor affecting your total cost. It can vary significantly between lenders and depending on your circumstances and the equipment you are financing.

-

Fees

Equipment finance can include a range of fees, such as establishment fees, valuation fees and early termination fees. These vary between lenders and can impact the overall cost of the agreement.

-

Equipment type

The type of equipment being financed affects the rate and terms available. High-demand or widely resold equipment, such as vehicles or common machinery, is generally cheaper to finance than niche or specialised assets that are harder to value or sell.

-

Equipment condition

Newer equipment often attracts lower interest rates, as it depreciates more slowly and holds a higher resale value. Used or older equipment may attract higher rates or require a larger deposit, as it represents greater risk to the lender.

-

Business finances

Lenders assess your turnover, profit, liabilities and trading history to understand repayment capacity. Strong cash flow, low debt and an established trading history can improve your rate and terms.

-

Business age

Newer businesses are seen as higher risk, which can lead to higher rates and stricter terms, while more established businesses with a proven track record are typically offered more competitive pricing.

-

Personal profile

For smaller or newer businesses, personal credit history may also be considered. A strong personal credit profile can improve approval chances and help secure a lower rate.

-

Balloon or residual payment

A balloon or residual payment reduces your regular repayments by deferring part of the loan balance to the end of the term. While this improves cash flow, it increases the final lump sum due.

Business loan calculator

Crunch the numbers to see what your repayments could look like

Your estimated repayments

$98.62

| Total interest paid: | Total amount to pay: |

| $1233.43 | $5,143.99 |

How much can my business borrow for equipment?

How much your business can borrow for equipment finance depends on a range of factors, with your revenue and overall financial position playing the biggest role. Lenders will also assess your industry, trading history and existing liabilities when reviewing your application.

The type and value of the equipment being financed will also influence borrowing capacity. Higher-value assets such as heavy machinery or commercial vehicles typically require larger loan amounts, while smaller purchases like office equipment generally involve lower borrowing levels.

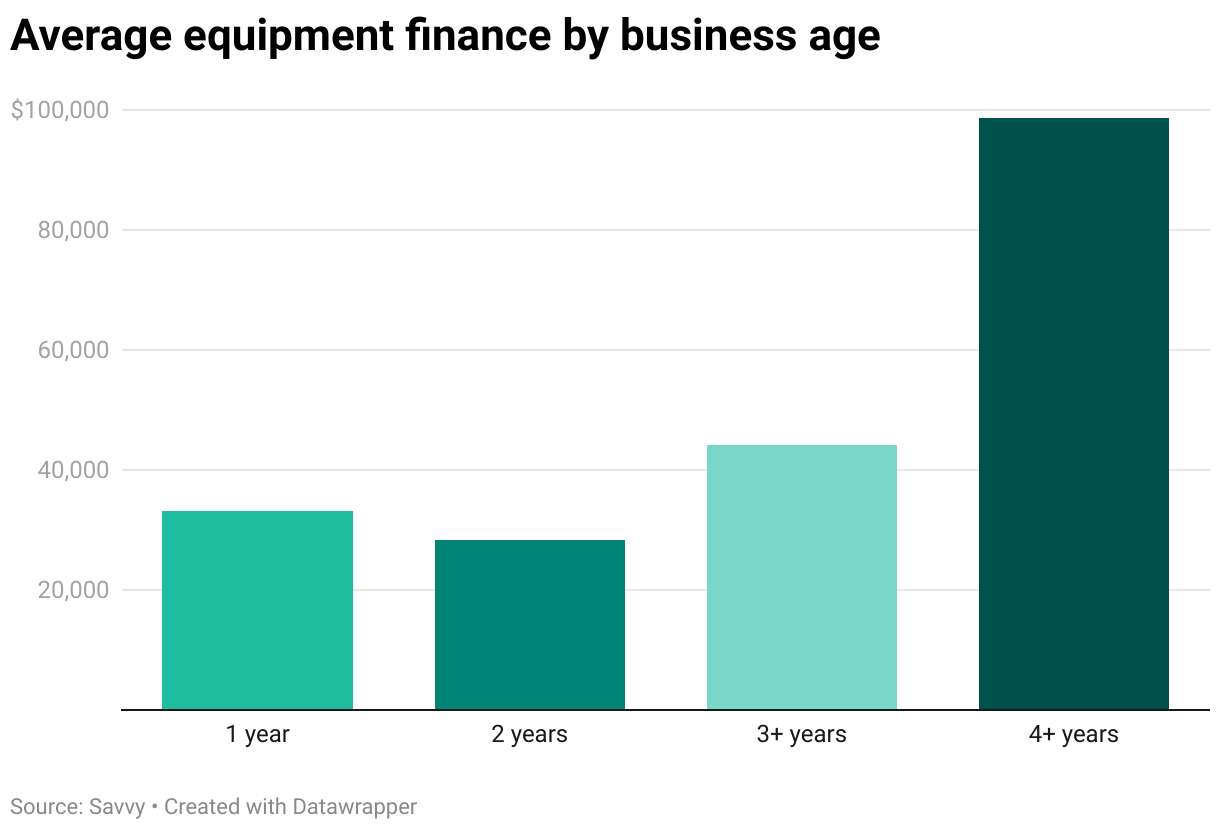

Our data shows that businesses with an annual turnover above $2 million tend to access the largest equipment loans. Here's a look at the average finance amounts by revenue for 2025:

| Applicant annual revenue | Average amount financed |

|---|---|

| Less than $200,000 | $37,122 |

| $200,000 – $500,000 | $53,782 |

| $500,000 – $1,000,000 | $77,014 |

| $1,000,000 – $2,000,000 | $91,710 |

| $2,000,000+ | $163,631 |

| Source: Savvy, 2025 | |

We also see that the longer a business has been active, the more they tend to finance – with the exception of first-year businesses, which often borrow more than those in their second year of trading. This likely reflects setup costs and the upfront investment needed to get established, combined with limited cash reserves and the drive to expand quickly. Beyond that stage, borrowing generally increases in step with growth and stronger revenues.

How to apply for equipment finance

-

Complete our online form

Provide key business and personal details and your desired loan amount.

-

Upload your documents

Submit the required paperwork through our secure portal.

-

We'll review your profile

Your broker will compare loans and lenders to find the best solution for your needs.

-

Finalise your application

We’ll help you complete the application and submit it to the lender.

-

Sign and access funds

Sign the agreement and receive funding for your equipment.

Why apply for a business loan with Savvy?

Are my equipment finance payments tax-deductible?

Yes, on a chattel mortgage, interest may be tax-deductible as a business expense. If your business is registered for GST, you may also be able to claim a GST credit on the initial purchase on your BAS.

With a finance lease, GST paid on lease payments can also be claimed as an input credit, reducing your GST liabilities.

It's important to note that you can only claim the business portion of your asset's usage. For example, if you bought a ute and used it for business purposes 70% of the time, you could only claim up to 70% of eligible expenses.

If your equipment is under $20,000 and you own rather than lease it, you may also be able to deduct the full cost of the asset through the instant asset write-off. This is an alternative to claiming gradual depreciation on business assets, freeing up more cash upon receiving your tax refund. The scheme was set to expire after the 2024-25 financial year, but the Australian Government has extended it until 30 June 2026.

Additional tax deductions may apply depending on your situation, so consulting with a tax professional can help you maximise potential savings.

Make the most of the instant asset write-off

"While the $20,000 instant asset write-off won’t cover larger equipment, it can still be useful for smaller business assets and accessories. Items like excavator buckets, ute toolboxes, small trailers or specialised attachments can qualify, helping you reduce your taxable income while upgrading essential equipment."

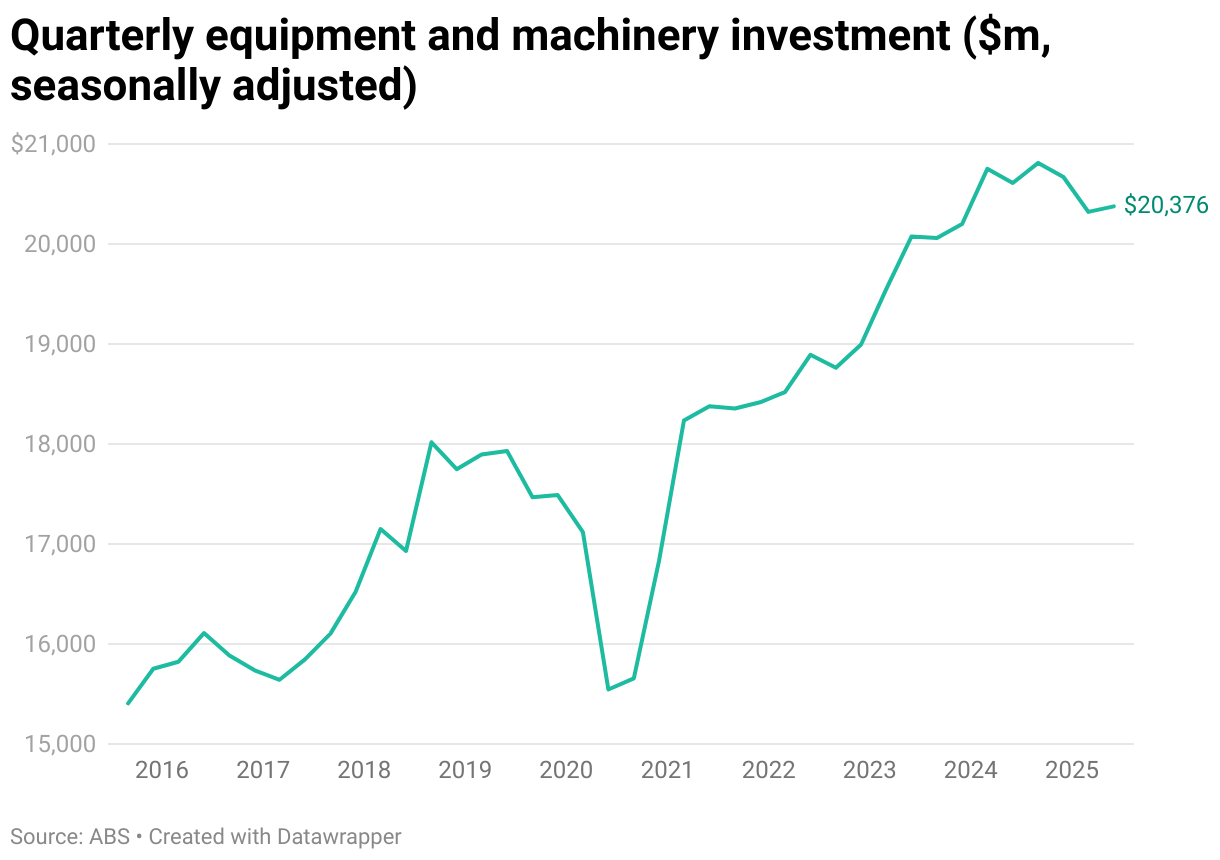

Equipment spending in Australia

In the past ten years, Australian spending on business equipment and machinery has grown steadily, reaching around $23 billion in the December 2025 quarter, according to ABS data – an increase of more than 40% over the decade.

Investment levels vary significantly between industries. Looking at the year-on-year results, while some sectors have seen declines, many have recorded strong increases in equipment investment between December 2024 and December 2025, pointing to broad but uneven growth in spending across the economy. Construction and other services have lagged over the period, potentially reflecting more challenging conditions in those sectors, including a slowdown in building activity.