What is a chattel mortgage?

A chattel mortgage is a secured loan used to buy a vehicle, machinery or equipment for your business. It can be used to finance a wide range of business assets, from cars, utes and trucks to larger pieces of equipment and machinery.

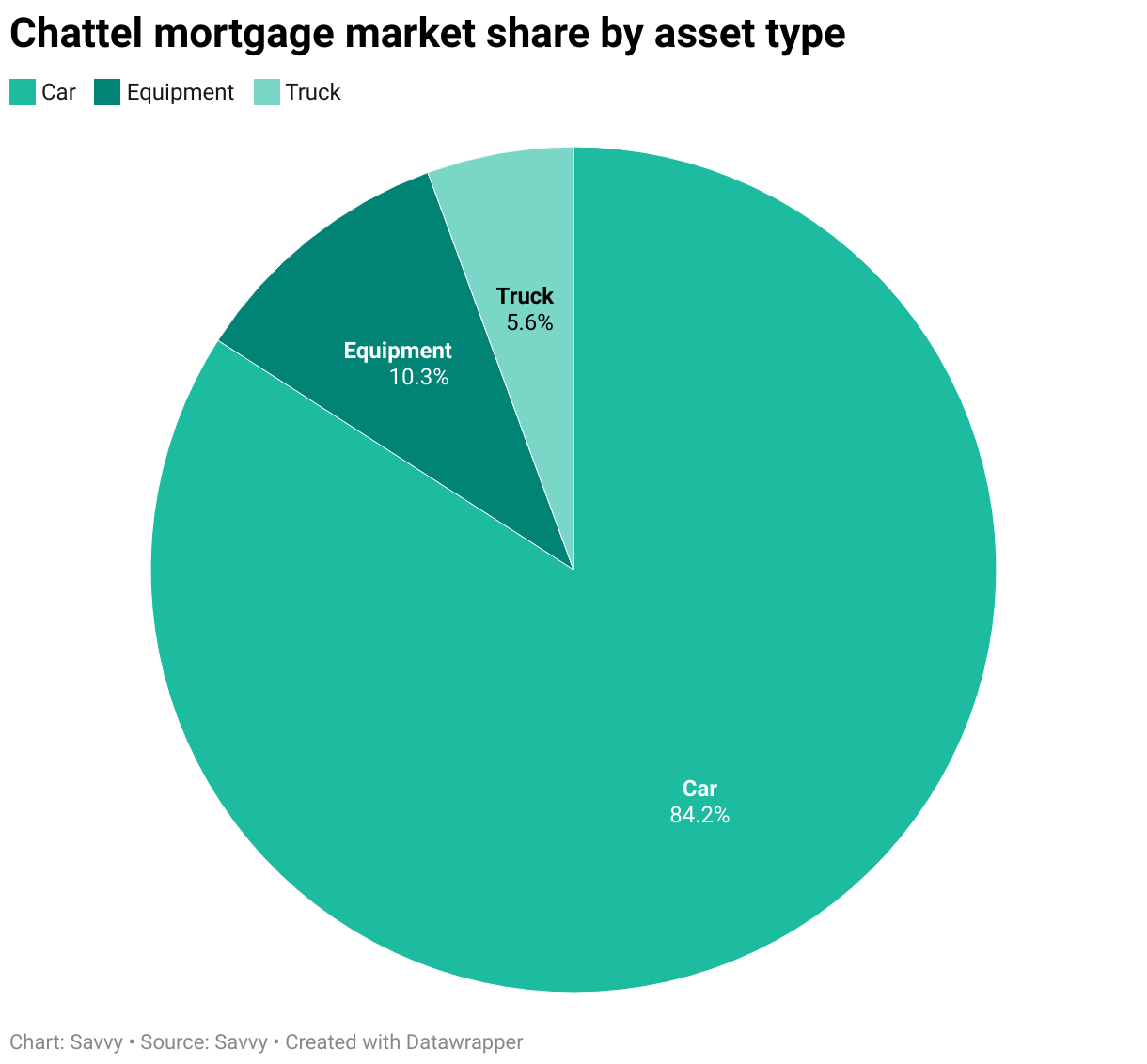

In 2025, commercial vehicles accounted for around 82% of approved chattel mortgages taken out through Savvy, with equipment and trucks making up the remainder, at 11% and 7% respectively.

As with other types of lending, you borrow money to make the purchase, then repay the amount borrowed with interest over an agreed term.

Under this arrangement, your business owns the asset from the start, with it used as security for the loan. This may help you qualify for a larger loan or a lower interest rate, but the lender can repossess the asset if you fail to meet your repayments.

This type of finance can be used to buy new or eligible used assets, with the loan structured around the purchase and your business’s cash flow.

Chattel mortgage interest rates

As of July 2026, these are the lowest available chattel mortgage rates available through Savvy.

Rates are indicative only and based on a business with an ABN registered for at least eight years, GST registration for at least four years, a 60-month loan term and a $50,000 vehicle purchase. Your actual interest rate will depend on factors including your business profile, credit history, financial position, the vehicle being financed, loan amount, term and the lender's assessment criteria.

How much will my chattel mortgage cost?

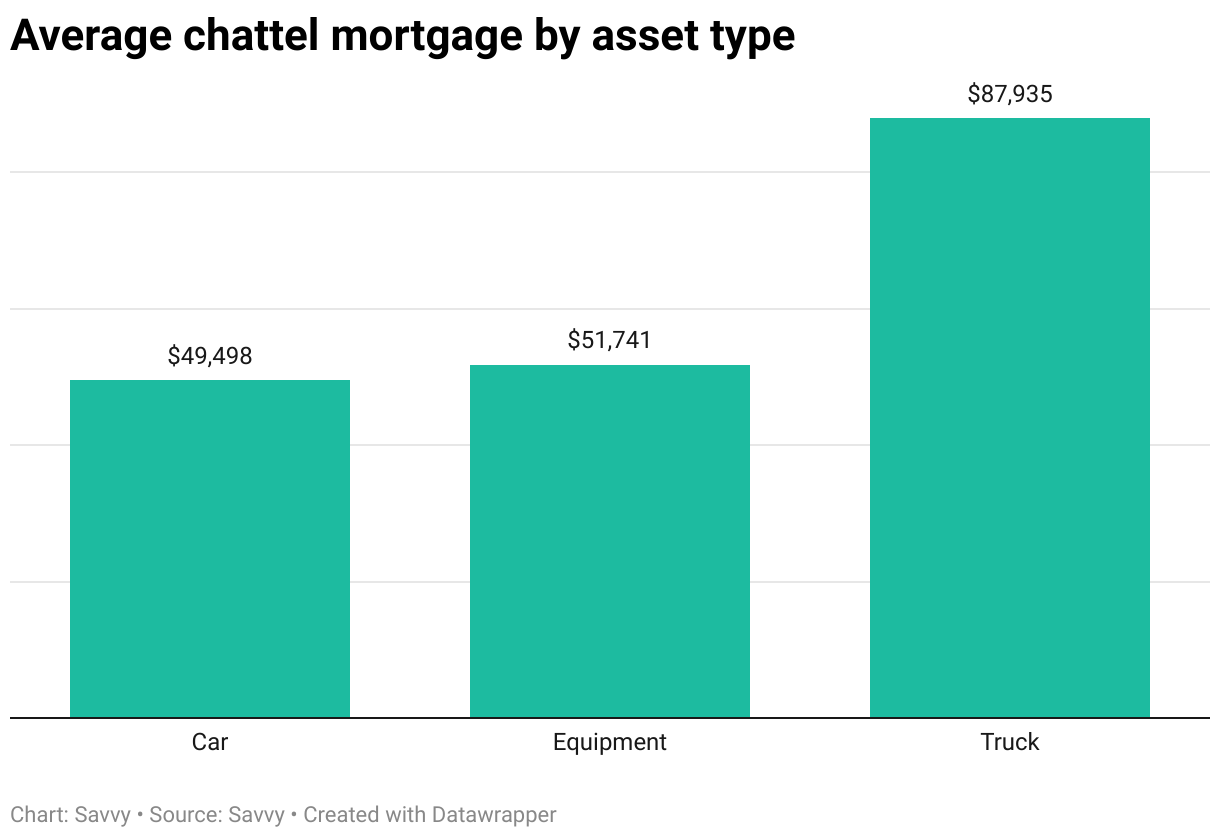

The average chattel mortgage taken out through Savvy in 2025 was $67,579 over a five-year term.

Loan sizes varied depending on the asset being financed, with truck finance averaging $96,424, compared to $62,864 for equipment and $62,055 for commercial cars.

However, the amount you borrow is only one part of the total cost of a chattel mortgage. Your overall cost will also depend on factors including the interest rate you receive, the loan term and whether you include a balloon payment.

Here’s how each of these could affect your repayments and the total amount you repay over the life of the loan.

Interest rate

Your interest rate is one of the biggest factors affecting the cost of your loan. Rates are tailored to each borrower and may vary depending on factors such as your credit history, your business's financial position and trading history, and the type of asset you're financing.

For example, on a $50,000 loan over five years:

| Interest rate | Monthly repayment | Total interest |

|---|---|---|

| 6.50% p.a. | $978 | $8,698 |

| 7.50% p.a. | $1,002 | $10,114 |

| 8.50% p.a. | $1,026 | $11,550 |

Loan term

A longer loan term generally reduces your regular repayments, but you'll usually pay more interest overall. A shorter loan term means higher repayments, but less interest over the life of the loan.

Here’s how that would look based on a $50,000 loan at 7.50% p.a.:

| Loan term | Monthly repayment | Total interest |

|---|---|---|

| 3 years | $1,555 | $5,991 |

| 5 years | $1,002 | $10,114 |

| 7 years | $767 | $14,421 |

Balloon payment

Choosing a balloon payment can reduce your regular repayments by deferring part of the loan balance until the end of the loan term. While this can improve cash flow, you'll pay more interest overall because a larger balance remains outstanding throughout the loan.

This is how different balloon amounts would impact the repayments on a five-year, $50,000 loan with a 7.5% p.a. interest rate:

| Balloon payment | Monthly repayment | Total interest |

|---|---|---|

| – | $1,002 | $10,114 |

| $10,000 (20%) | $864 | $11,841 |

| $15,000 (30%) | $795 | $12,705 |

The power of the balloon

"Balloons are common practice for business owners, especially those who look to update their vehicle every two to three years. A good broker can tailor your balloon payment to fit your preferred budget."

Chattel mortgage repayment calculator

Why apply for a business loan with Savvy?

Chattel mortgage tax benefits

A chattel mortgage may offer several tax benefits when the asset is used for business purposes. Depending on your circumstances, you may be able to claim:

- Interest charged on the loan

- GST paid on the purchase price

- Depreciation in the asset’s value over time

Note that you can only claim the portion of these expenses that relates to business use. For example, if a vehicle is used for business purposes 75% of the time, you will only be able to claim 75% of the eligible expenses. If the asset is used exclusively for business, the full amount may be claimable.

If you’re unsure what or how much you can claim, speak to an accountant or registered tax professional to confirm what you can claim before completing your tax return.

Chattel mortgage pros and cons

Pros

-

Borrow up to 100% of your asset’s price

A chattel mortgage may allow you to finance the full purchase price without using a large portion of your business’s cash reserves.

-

Own your vehicle or equipment from the start

Your business owns the asset from the beginning of the loan, giving you more freedom over how it is used (though some modifications may require the lender’s approval).

-

Enjoy tax benefits

Depending on how the asset is used, your business may be able to claim deductions for interest, depreciation and GST.

Cons

-

The asset can be repossessed

Because the loan is secured against the asset, the lender can repossess it if you fail to meet your repayments.

-

Early repayment fees may apply

Some lenders charge early termination or break fees if you repay the loan before the end of the agreed term.

-

The asset must meet lender requirements

A chattel mortgage is tied to a specific vehicle or piece of equipment, which must meet the lender’s age, condition, value and eligibility requirements.

How to apply for a chattel mortgage with Savvy

-

Apply online

Fill out our short form to tell us what you’re after.

-

Submit your documents

Upload your documents to our secure online portal to verify your profile.

-

Chat with your Savvy finance broker

We’ll give you a call to discuss your commercial finance options.

-

Submit your application

Your application will be sent to your chosen lender for formal assessment.

-

Receive funding

Once you’re approved, all that’s left is to sign off and secure your asset!

How does a chattel mortgage compare to other types of finance?

Businesses have several ways to finance a vehicle or piece of equipment. The right option will depend on whether you want to own the asset, how long you plan to keep it and what you want to happen at the end of the agreement.

Here’s how some common alternatives to a chattel mortgage work:

| Finance option | How it works |

|---|---|

| Finance lease | The finance provider purchases and owns the asset, while your business makes regular payments to use it. A residual payment is included at the end of the term, which you can pay to purchase the asset, refinance or cover by selling or trading it in. |

| Operating lease | The finance provider purchases and retains ownership of the asset while your business pays to use it for an agreed period. The business never takes ownership, and the asset is returned at the end of the lease. |

| Hire purchase | The finance provider purchases the asset and hires it to your business. Your business makes regular instalments, with ownership transferring after the final payment is made. |

When should I choose a chattel mortgage?

A chattel mortgage may be a suitable option if the asset will be needed for the ongoing operation of your business rather than for a short-term or one-off project. It allows you to spread the purchase cost over time while using the asset to help generate income for your business.

Financing a vehicle or equipment through a chattel mortgage can also give businesses the flexibility to customise the asset and any usage restrictions. If long-term ownership is your goal, a chattel mortgage is often one of the most cost-effective finance options available.